|

|

|

|

03 October, 2015: Created

02 February, 2016: Added P.III.S

25 September, 2016: Added link to cash graphic

05th November, 2019: Added prefix.

24th October, 2022: Added P.IV.S, on role of non-term life insurance when dealing with gifts and endowments.

30th October, 2022: Modified P.III.S, regarding author's own common-stock investments.

09th November, 2022: Added P.V.S detailing the mechanics of working with The National Pension System (NPS)

28th December, 2022: Added P.VI.S on mechanics of handling large sums of cash, including endowments.

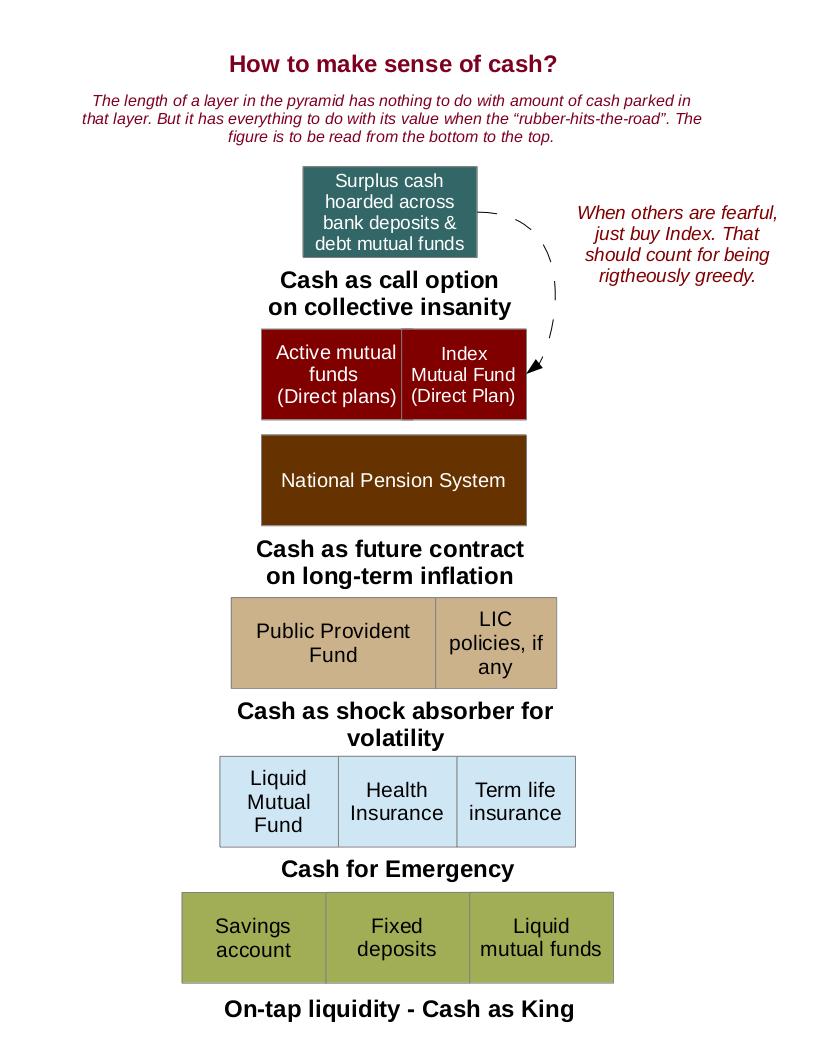

For those in a tearing hurry this visual may serve as an effective executive summary.

Along-side three rules:

1. Safeguard what you have.

2. Compounding is a product of two things: delayed gratification & behaviour of financial markets. You can control only the first.

3. The analogy of drip irrigation works well: whatever money you park in long-term instruments, do it slowly but consistently.

Update, 03th November, 2019: When the following page was penned, the author was at a certain point in terms of his personal finances. Three years hence, the balance sheet has expanded slightly. The author's fundamental investment approach has not changed except to make the National Pension System an integral part of his portfolio. Indeed it is the first pillar on which all other longer-term investments are being built.

In the meantime, the author has had a chance to deal with informal queries of a variety of women: widowed, separated, old age, etc... The term women matters because, financially, in India, they are the most vulnerable. In dealing with their queries, the author has come to the conclusion that the safest portfolio for most persons is PPF+NPS+One Large-cap actively managed fund. The allocation can vary depending on one's time preference. This, incidentally, is very much along the lines of how the author has structured his portfolio. It is low-cost, almost nil maintenance, and easily understandable by anyone willing to decode the three products, and incidentally as tax efficient as you can get when investing for the long-term.

It will not be the portfolio that will fetch you above average returns, but will provide a stable and dull ride over one's life. As far as investing goes, that is all one should ask and expect.

Those nearing 70 and above 70, should stay with a set of fixed income instruments + Annuities + Highly conservative allocation to a large cap actively managed fund.

There is a general caution for everyone: the structure of Indian equity markets has changed partly due to demonetisation and partly due to the cardinal stupidity committed of popularising SIPs amongst the general masses. The author has heard things like: should I invest in PPF or do a SIP? That is, there is little understanding for many of what really investing in long-duration financial markets is about. Just because a word has been popularised ad-infinitum, people have taken it as an article of faith. This stupidity of the massess is most likely going to lower the next 10 year potential returns than would otherwise have been the case. The fund houses are of course laughing their way to the bank.

"It was little short of nonsense for the stock market to say in 1937 that General Electric Company was worth $1,870,000,000 and almost precisely a year later that it was worth only $784,000,000. Certainly nothing had happened within twelve months' time to destroy more than half the value of this powerful enterprise, nor did investors even pretend to claim that the falling off in earnings from 1937 to 1938 had any permanent significance for the future of the company. General Electric sold at 64 and seven-eights because the public was in an optimistic frame of mind and at 27 and one-fourth because the same people were pessimistic. To speak of these prices as respresenting "investment values" or the "appraisal of investors" is to do violence either to the English language or to common sense, or both."

---Benjamin Graham and David L. Dodd in the chapter "Introduction to Second Edition", Security Analysis (Sixth Edition), Tata McGraw-Hill edition.

"From May 1995 through March 2009, despite two intervening speculative bubbles, the total return of the Standard & Poor's 500 Index lagged the total return of risk-free Treasury bills. This was also true for the period from August 1959 through August 1982, as well as the period from August 1929 to August 1945. Indeed, during the 80-year period from 1929 to 2009, the S&P 500 took three long, interesting trips to nowhere, accounting for 53 of those years (1929-1945, 1959-1982, 1995-2009), underperforming risk-free Treasury bills after all was said and done."

---John. P Hussman, in the annual report of Hussman Funds, dated 30th June, 2020.

"...2 years ago we were selling at 10 times revenue when we were at $64. At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 years straight in dividends. That assumes I can get that by my shareholders. That assumes I have zero cost of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees. That assumes I pay no taxes, which is very hard. And that assumes with zero R&D for the next 10 years, I can maintain the current revenue run rate. Now, having done that, would any of you like to buy my stock at $64? Do you realize how ridiculous those basic assumptions are? You don't need any transparency. You don't need any footnotes. What were you thinking?"

---Scott McNealy, co-founder and CEO of Sun Microsystems to Bloomberg in 2002 reminising on the dot-com mania, sourced from Dispelling myths in the Value vs. Growth debate, GMO quarterly newsletter, Q2, 2021.

"In a rising market, everyone makes money and a value philosophy is unnecessary. But because there is no certain way to predict what the market will do, one must follow a value philosophy at all times. By controlling risk and limiting loss through extensive fundamental analysis, strict discipline, and endless patience, value investors can expect good results with limited downside. You may not get rich quick, but you will keep what you have, and if the future of value investing resembles its past, you are likely to get rich slowly. As investment strategies go, this is the most that any reasonable investor can hope for.

The real secret to investing is that there is no secret to investing. Every important aspect of value investing has been made available to the public many times over, beginning in 1934 with the first edition of Security Analysis. That so many people fail to follow this timeless and almost foolproof approach enables those who adopt it to remain successful. The foibles of human nature that result in mass pursuit of instant wealth and effortless gain seem certain to be with us forever. So long as people succumb to this aspect of their natures, value investing will remain, as it has been for 75 years, a sound and low-risk approach to successful long-term investing

"

---Seth A. Klarman, Boston, Massachusetts, May, 2008 in a commentary before the preface of the Sixth Edition of Security Analysis by Benjamin Graham and David L. Dodd, Tata McGraw-Hill edition.

"Benign neglect, bordering on sloth, remains the hallmark of our investment process." ---Warren Buffett

"An investment operation is one which upon thorough analysis promises safety of principal and a satisfactory return." --- Benjamin Graham and David L. Dodd's definition of investment in Security Analysis to assert its distinction from speculation (which by definition implies that what is not an investment is a speculation.)

"The world has largely lost of sight of that distinction (between investment and speculation). The treasurer of Orange County, California, thought nothing of borrowing heavily and then speculating with the funds for public schools, roads, and waterworks on esoteric interest-rate derivatives, as a consequence of which the county recently went into bankruptcy. Indeed, the notion of intrinsic value is itself something of a lost ideal. In a world of shifting benchmarks and changing "spots," value is not intrinsic but ephemeral; the painting cannot be appreciated until the critic weighs in, and beauty is truly up to the beholder. In Orange County, beauty was whatever the treasurer or Merill Lynch, his broker, said it was. Neither really knew, and therefore both were willing to speculate. At the other end of the spectrum, this lack of conviction results commonly in cowardice and mediocrity.

If we have lost the people with Emersonian inner conviction, it is because we have lost the fixed stars that formerly guided them. The modern relativism has reduced us all to being timid specialists, peeping out from cubbyholes marked "growth" and "derivative." For similar reasons --- the lack of intrinsic value systems - educators waffle and juries seem unable to convict. They retreat, as it were, into ambiguity, complexity, and cacophony. Where one conviction is lacking, a thousand opinions will do --- indeed, they become a necessary recourse. Our captains seem the smaller for it, not only on Wall Street but in industry, education, government, and public life in general. (pg. 421)

...

Today, the frenetic trading at Wall and Broad may be seen as a metaphor for the rapidity with which once-firm social connections, to job, neighbourhood, family, civic affiliation, and the past itself, become unglued. And unglued each day all the faster. When Andy Warhol predicted fifteen minutes of fame for each of us, he did not get the half of it. In these restless times, it is not only our fame that disappears in a quarter of an hour, but, seemingly, every relationship that once was enduring or valued for its ongoing character. Professional partnerships splinter apart, athletic heroes desert their teams, employers overhire and then overfire, and even our universities, the supposed repositories of our past, race to reinvent the canons that had served for a near-millennium. In our daily walks of life, the faces on the trolley change overnight. Investors seek their exit strategies, but they are hardly alone. Viewed in ths light, Wall Street's mania for shuffling paper is only the most blatant sign of the general rush to put a price on once-lasting commitments. This is why Buffett filled a hollow. More than most, he reclaimed the rewards that spring not from trading commitments one for the next, but from preserving them. (pg. 426)

--- Buffett, The Making of an American Capitalist, Roger Lowenstein, 2008 Random House Trade Paperback Edition, USA; originally published in 1995.

-6. There is more to life than generating money. In fact, everything that is of any importance in life precedes making and conservation of money. Then what is the use of money, and more generally, wealth? The answer is: to allow one to avail the maximum freedom of choice that one's circumstances allow. Investment, or more generally, financial planning, in that context is a means to create and safeguard that freedom of choice. Every monetary decision should be weighed against a simple consideration: will it improve or diminish my freedom of choice as of today?

-5. What is this 'freedom of choice'? Taken in its broadest sense, it can only mean one thing: a deep psychological comfort with one's present state of existence. The greater your mind is unagitated the better one's well-being is. Anything that binds the mind is not to be pursued without a lot of critical scrutiny. Choice of one profession over another may be deemed a freedom of choice because it leads to a 'liberating feeling'. This feeling is due to not taking part in things that one is really averse to. This in turn leads to mental stability and a deeper, unfelt level of joy. The earlier you try get to this the better it is. Like Warren Buffett famously said, why would you delay having sex till old age?

-4. In context of personal finance it means that management of personal finance should be done in a manner that does not lead to enhanced agitation of mind. Else, while your bank balance is growing on the left side of the balance sheet, on the right side off-balance sheet liabilities in form of enhanced medical expenditure, family issues, disputes with strangers on account of property etc. are accruing steadily. There is a sweet spot beyond which money is an oasis in midst of a very harsh desert. Refuge in the oasis will not save you from the unpredictable sandstorms in the chillingly biting night.

-3. Thus it is important to be very clear: is your problem of management of personal finance a problem of plenty or a problem of scarcity? If it is a problem of scarcity the likelihood of being a better financial manager is higher: one's sharpness, alertness and acumen will be more involved. If it is a problem of plenty then the likelihood of being lazy, rash, playful, an excel-sheet-investor will be higher. Even if one has plenty, one has to invest with an attitude of scarcity. That is, value each rupee that is 'invested' --- as if it is the last rupee that you are going to put in.

-2. In the specific context of investment there are no categorical truths except one: compounding works to maximum advantage provided one invests in proportion to the margin of safety available. (It is the difference between investing Rs. 5,000 when Nifty PE is 20 from investing Rs. 10,000 when Nifty PE is 15). Everything else is circumstantial and temperamental. The forced discipline of SIP for one man can be a liberating experience from the tyranny of unchecked spending while for another it may be an unnecessary shackle that does not allow a fine-tuning of how much to invest and when.

-1. Managing money is hard work. Multiplying money the right way is extremely hard.

0. Put another way: in the world of finance investment is short-hand for 'temperament'. An act of investing is an act of seeing one's own temperament at play. Much like the act of writing is an act of seeing one's creative faculties at play. An act of playing a sport is an act seeing one's physical dexterity and mental acumen at play. Thus there is always a danger that an act of investment will turn into one of speculation: because there is a fine line between 'playing for a purpose' and 'playing for fun'. Lets play for a purpose. Depending on one's temperament one's style of playing may change.

Thus, what is stated below is a 'style'. It is not a 'formula'.

1. An act of investment will follow an act of insurance and will not be at the cost of insurance.

2. Amount ear-marked for investment will be accrued as a function of post-tax savings and not come at the cost of cutting down on pre-tax operating expenses that are required to lead a thrifty but comfortable life.

3. One will exert oneself ardently and with sincerity to pay the maximum tax possible taking appropriate advantage of the exemptions and provisions available under the Income Tax Act. By the term 'appropriate' it is meant that the tax provisions to be taken advantage of should be fully in line with the source of one's income and reflect the way one's business truly operates. The operation of business should not be influenced by choice of specific tax provisions but vice-versa.

4. The choice of a particular investment will not be influenced in any material degree by the tax treatment associated with the gains from the investment. An investment decision will be determined by the specific real-world need it is meant to address.

5. The objective of an investment decision will be to conserve and protect one's hard-earned money against the vicissitudes of fortune which manifest themselves as inflation, temporary loss of job, partial or full inability to work, or a black-swan event at a personal level, i.e. death.

5.1 As a corollary, if one is in possession of large heritance, or for whatever other reasons, happens to find oneself a favoured child of serendipity then one will hire a professional fund manager to achieve a specific aim. One hopes that that aim will be to not use the sum for purchase of an Audi among other things but to secure the next 2 generations of one's family and contribute the rest to those who really need it. In this, one will benefit from periodic remembrance of the fact that one in five Indians live in a state of deprivation that completely nullifies the definition of the term 'humanity'.

6. Investment will not be a substitute for making a living through hard-work in one's area of competence. If that area happens to be 'investing' then great, else one has to be firmly content with what one can honestly extract out of the employment-market for the skill that one possesses. At no point should gains from investments lead to accumulation of lethargy, inertia, sloth, torpor and a general unwillingness to stay the course. However, investment can be used to provide a platform for pursuit, full-time or part-time, of more creative but socially constructive pursuits.

7. Purchase of physical assets, such as property and gold, does not constitute an act of investment. Purchase of such assets will only be on a 'consumption' or a 'need' basis. Even if such an asset is purchased when there is no real need for it, it will be treated as an artificial store of excess cash and not be carried on the books on an 'investment' basis.

8. From 5, 6 and 7, it follows that an act of investment will concern itself with instruments that are directly linked to profits generated out of constructive economic activity. (It is not practical to strictly enforce this rule. Lets say one is invested in a mutual fund that tracks the stock market index. What is the guarantee that each of the constituent companies that comprise the index are generating profits only out of productive economic activity. Unfortunately, there is no such guarantee. However, at a personal level, one can try to the extent possible to not indulge in actions that are directly adding to unproductive economic transactions or, in more explicit terms, resulting in a simple exchange of money changing hands.)

9. A significant majority of the investments will be in financial assets of government and businesses based in India (not necessarily Indian). This is premised on the belief that investment is an act of reposing one's hard-earned money to someone else. In that 'choice' of someone else it is better to repose one's trust in a known devil rather than a potentially unknown angel. In addition, money needs to flow into the immediately surrounding economy as far as possible and not be chasing, and in the process of confusing, dreams of people of distant lands. The NRIs would need to take special note of this.

10. The purpose of investment first and foremost will be to achieve and preserve an asset-liability equilibrium at all points of time. Only secondly, will its purpose be to generate an out of turn real rate of return. The term 'liability' means actual financial liabilities standing on one's book today as well as the ones that are off-balance-sheet in form of needs of family, thoughtless actions taken in the past that are likely to make their impact felt at any point of time and sundry others.

11. Investment will be into products that one understands, not in ones that one does not understand or that fall outside one's zone of comfort. Thus, if product X has historically performed very well compared to product Y, but if one does not understand product X but understands product Y, then one will invest in product Y. For example, if there is a mutual fund scheme that invests in large-cap stocks and another that invests in an Index fund (with lower returns compared to the large-cap scheme) but if one is more comfortable with an Index Fund in terms of simplicity of understanding then one will put one's hard-earned money in an Index Fund. Having said that, though, if one is willing to spend enough time to educate oneself, then of course, this suggestion will seem outlandish.

12. Every act of investment will be such that upon one's death the rest of the family is able to understand and use the investments to their advantage. That is, the complexity of investment will be determined by the level of financial acumen of the family. There should be no need for an outside advisor to decode one's investments. Alternatively, if one indeed wants to build a sophisticated portfolio investment, then one has to be good at maintaining detailed notes and documentation to ensure that the beneficiaries at least have a documented point of reference to start from.

13. Following from point 11, the following order would be adhered to all times to partition one's investment holdings: a) a pool of emergency reserve, b) a pool of 2 month working capital need, c) a pool of 12 month cash-flow requirements, d) all other remaining fund to be treated as a holding fund to be gradually converted into appropriate-duration instruments to meet future liabilities: those in line-of-sight today as well as those whose contours are being seen through the late evening mist on the horizon.

14. The pool of emergency reserve will be in form of 2 simple fixed deposits of equal value and as large an amount as possible.

15. The working capital reserve would be in form of a treasury fund if one is comfortable with the notion of liquid mutual funds.

16. Pool of 12 month cash-flow requirement would be in form of a ultra-short-term liquid fund. It would include an amount to meet at least the following cash outflows over at least a six month and preferably a 12 month period: a) insurance premium payments, b) principal portion of EMI repayments, c) any SIPs running on longer-duration instruments apart from the monthly household expenses.

17. The holding investments will also be kept in form an ultra-short-term liquid fund and transferred either in lump-sum or incrementally onto longer-duration instruments (PPF, Common-stock SIPs, Debt Fund SIPs, etc.).

18. As far as investment in common-stock instruments is concerned, unless one understands how to decode individual stocks or the market trends, one will stick to simple equity mutual funds from reputed and long-standing asset management firms.

19. One will not time the equity or debt market on a monthly basis. It is so simple to follow that you just can't possibly go wrong except not heeding to it.

20. One will commit only those funds to equity markets that are available after covering at least 3 years worth of entire set of personal liabilities. Since there is no realistic way of accurately assessing one's liabilities over a 3 year period and beyond, this is another of saying be prudent but consistent in one's commitment to equity markets. The principle applies in general to any high-risk instrument where there is a clear risk of principal erosion in the short to medium term.

21. The post-tax profit that one earns will be appropriated and distributed as follows: a) a portion to be transferred to emergency reserve, b) a portion to be given as gift to family (akin to dividends to shareholders of a company), c) a portion to be kept aside for building one's own capital base for personal welfare spending on one's staff and associates at home and office, d) a portion to be transferred to 12 monthly reserve, and e) the balance transferred to reserve for holding funds to be invested in longer tenure securities and instruments.

22. Keep all professional advisors at an arms length. Don't listen to stories not because the stories are false but because an act of investment does not need stories. It is very simple and should be kept as such: there is either fixed value investment or common-stock (equity) investment. One can create infinite combinations using the two. It is better to create one's own rather than be sold one by an advisor. Even if you go for a mix, make sure you know what are the non-investment (behavioural and psychological) reasons for choosing a 'heady cocktail' instead of a 'solitary red or blue wine'.

23. Finally, if at any point of time one feels that one has missed out on an easy opportunity to make money, one should remember: the fact that one was in a position to think about making money from a supposedly easy opportunity is itself a great boon compared to those many who do not have the luxury of entertaining such a thought. The freedom to think about an 'opportunity' is a reward in itself. Any further material reward is a bonus. The gift of contentment is the highest wealth possible for those who already possess more than what they really need.

24. In summary,

24.1 Rule 1: Trust no one with your money, including yourself.

24.2 Rule 2: Know for a fact that you know no facts about the future. Stepping out of your home you could be hit by the next vehicle that is speeding by.

24.3 Rule 3: Develop a habit of always remembering Rule 1 and Rule 2.

24.4 Rule 4: Rule 3 means that manage your money by rules and not by emotions.

24.5 Rule 5: To execute Rule 4 well means keeping all other rules of money-management simple.

24.6 Rule 6: Rule 5 will happen if you do things slowly and over a period of time. It takes an instant to create something complex and ages to simplify it later. Why run when you can walk at your leisure taking note of every leaf and sound in the garden. Remember: either you are dead today or you have a long way to go. There is no such thing as I will be dead in 20 years or I will retire in 20 years.

24.7 Rule 7: Don't spend your time worrying about improving your quality of life. If you are reading this on a reasonably expensive device, your quality of life is just fine. Figure out how to improve quality of your happiness. Money is brilliantly useless at that.

24.8 Rule 8: This is the most important rule. Keep meticulous diary of your investments and learn to prepare a summary balance sheet. Rather than doing mental accounting or allowing financial planners to construct your balance sheet, make one of your own. It takes roughly Rs. 50 for the diary and Rs. 10 for the cheapest and most reliable ball-point pen. Once a month make entries of the investments that have happened. You will save tons in advisory fees. And more importantly, it is a psychological fact: anything that can be seen clearly (like numbers) arouses less fear than a vague mental image of the same. Lack of clarity is the root cause of confusion. Confusion sustained by attachment greases fear.

24.9 Rule 9: When in doubt go back to the top of the page and read the whole page again. Rest assured, it will deliver more long-term value than facebooking, or worse still, trying to fish out the latest way to make money. This activity will certainly qualify as a 'value-investment' rather than 'speculation'. You will make Benjamin Graham and David L. Dodd proud. Their tacit approval could be your first value investment. Being value-oriented is so simple, isn't it?

P.S: How much of one's hard-earned money should be really committed to common-stock (equity) investment? An analysis of historical risk and return could provide one answer to that question. But for most people, that kind of answer would still leave lingering doubts because most people are not investing to substitute their earnings but investing to safeguard their earnings. Keeping this distinction in mind at all times, it is helpful to note that the purpose of any money is to be there when you need it. Long-term capital appreciation is one thing but finally, when the rubber hits the road you need that cash when you need that cash.

So, one principle can be: keep that amount in equity so that even if all of the equity portfolio is wiped out, it is not going to impair your ability to discharge your critical financial liabilities and responsibilities (short, medium and long) in any substantive manner. You can still sleep with the same state of mind that you did on the night before the market completely collapsed and can continue to sleep with the same equanimity even if the markets remain in that state for a prolonged period of time.

For example, lets say that in 2008-09 (when the sub-prime crisis happened and the Indian index took a sharp nose-dive) you had planned for purchase of a house. And lets say that a substantial, over 50% of your financial savings were parked in equity. It was actually an opportune time to buy a house given that the real estate prices had also dipped noticeably. If you were in your 30's then you would not have managed to accumulate substantial savings as you would still be in the first leg of your career. With half of your portfolio reeling under sub-prime pressure you were left with a dilemma: House prices are down. If I can manage to gather enough capital to put a down-payment and then apply for a loan it would be great. But the equity portion is down in the dumps. I know it will recover over the next year or so. But by then would the house prices hold at this level? Probably not. So, to take advantage of this capital opportunity should I raid my debt portfolio? And say I break my debt portfolio and the market takes more than a couple of years to revert to the mean, till then do I have enough liquidity available to meet emergency requirements and near-term cash-flows? Also, do I have employment security? Not many people would have come out of this series of questioning with absolute calm. At such a point, at least some of them would have wished for not staking their honour to the market to the extent they did.

Of course, even if someone had over 50% of one's portfolio in equity and it collapsed and that someone was still intent on buying a house, that someone would reach out to parents, friends and sundry to get that down payment going. Maybe that someone would be lucky of having some inheritance or some pot of gold to sell. And so on. But why do all this when a more conservative financial allocation may have ensured that that someone would not have been in this position to begin with? Why buy a home with a down-payment that is leveraged? Of course, endowments and gifts from family are not looked upon as a debt to be banked upon after much consideration but as a right. There is a strategic approach to conducting one's financial affairs and there is a jugaad approach to conducting it. Depending on one's temperament and sensibility one will be preferred over another. It should be clear by now that these principles are not fit for the 'jugaad' mentality (which is mistakenly called 'being entrepreneurial' nowadays).

There is another way to think about equity if the aim is to safe-guard, conserve, protect and preserve one's earnings. It is possible to think of investment in equity as a quasi-hedge on the investment on the debt portion of the portfolio. Particularly, hedge against inflation and hedge against ability to skim the cream of the market when the market is generous enough to offer itself to all & sundry (like what happened in the run upto the Lok Sabha elections of 2014). It is an utterly foolish man who will say no to free money on the table. But it is also an equally and utterly foolish man who will think that free money is available at all times.

So, in concrete terms what is the answer? Remembering at all times that personal investment entails investment to meet financial liabilities and not investment for the sake of investment, a ratio of 3:1 in debt and equity under the kind of interest rate environment that India has seen makes sense today. Two factors can (and not necessarily should) change this allocation.

One is the movement in interest rate. A decline in interest rate should not imply an automatic switch to the markets. One has to really observe how the markets are behaving to effect a change in this ratio. If the scales are weighed more sharply in favour of the equity market then one can make a gradual change to say 2.5:1 to the maximum of 2:1. At no point is it psychologically advisable to invest one rupee in the market for every one rupee in the FD + PPF + LIC + Debt funds + whatever else qualifies as sound debt investment.

Except when a 2008 happens. When the index really nose-dives and one is clear about why the index has nose-dived and what is going to happen thereafter, it makes absolute sense to be opportunistic and with absolute equanimity change that ratio rapidly to 1.5:1 and then wait for the sun to shine, assuming of course that there are no major financial liabilities due in the interim. If they are, then the ratio can be adjusted accordingly.

But people who can understand the market to this deep extent and for whom all other factors are in perfect harmony for them to make such a dramatic shift are few. Most of us should restrict ourselves to put 50 paise in the market for every one rupee we hold in our debt portfolio during such times.

There is one scenario where investment in equity would make eminent sense for a man of and with family. If he was wise and astute enough to forsee and endowed financially to participate in major structural changes in the economy. Two such instances come to mind in India. The moment of 1991 when the economy was 'liberalized' and the arising of the internet era. The first one was much safer to bet on than the second as far as expansion in corporate profits was concerned. It was a no-brainer that if one would simply invest in the index at such moments, one is likely to see a very robust growth over a decade and more. Thus, for someone who would have been a wide-eyed 25 year old in 1991, today in 2015, at the age of 49, he or she would be a very contented individual as far his or her choice to invest a substantial portion of his portfolio in equity would have been concerned.

The same however cannot be said of those who would have bet on the internet boom. It is difficult to say to what extent it has contributed to the growth of corporate profits today and whether that impact has been substantial or is still to be realized. So the man of and with a family would have stayed invested in one structural adjustment (1991) and stayed away from the other (2000+).

When is the next structural adjustment going to happen? The only answer for the man of family is "God knows but I am sure he does not care much". This also means that neither should the man of family also care much. If he senses such an adjustment under-way then depending on his or her intellectual capacity and stage of life he or she is at he or she can place a calculated bet. Till then, it is better to view common-stock investment as a hedge on the rest of the portfolio and a means of skimming the market when need be.

To keep coming back to the same point: it is far better to lead a life without seeing a significant erosion in one's principal than a life that sees a significant uptick in return but with a constant underlying worry whether is any of this going to really stay and what if it disappers as fast as it came?

To quote: "The one thing I will tell you is the worst investment you can have is cash. Everybody is talking about cash being king and all that sort of thing. Cash is going to become worth less over time. But good businesses are going to become worth more over time. And you don't want to pay too much for them so you have to have some discipline about what you pay. But the thing to do is to find a good business and stick with it. We always keep enough cash around so I feel very comfortable and don't worry about sleeping at night. But it's not because I like cash as an investment. Cash is a bad investment over time. But you always have enough so that nobody else can determine your future essentially.." --- Warren Buffett (emphasis added).

P.II.S: Investments in mutual funds: An investment in a mutual fund is an investment into the management culture behind that fund. It is a little brutish to rank mutual fund schemes from sundry houses in one sheet and then select the top-performing ones and repeat this exercise annually in the name of portfolio re-balancing. Rather than spend time researching stocks or mutual fund schemes, spend that time understanding the management culture that drives the fund house, its investment philosophy and especially the character and make-up of people behind it. It is possible to get a fair idea through the interviews given by the fund-house managers. Ideally, a walk inside a mutual fund office would reveal a lot more. Apply the same process that a mutual fund team applies before investing in a particular company. And if you like a particular fund house stick with that. It makes sense to put all your eggs in one or at most two baskets. Doing Index Investing and SIP is not that passive as one thinks it is. It is 'passive' with respect to taking a bet on the market. But before getting into the passive-mode there is a lot of activity that seems to be needed to really zone down on the right fund house. The right fund house is like the right stock. If you stay with it long enough you may not get rich quick but you will surely sleep well and leave behind a tangible asset in form of solid mutual fund unit holdings for the subsequent generation. Those are any day better than leaving behind property that is a genetic craze in India.

P.III.S: Usually, when directing money into equity schemes run by mutual fund houses the following sequence of steps shoud help reduce confusion and promote clearer thinking. For each step identify the set of options at hand. Usually one has a gut feel about which of these options is the one that makes sense. For the other options compare them against this 'gut-level' option by asking a simple question. If I make a shift from my gut option to any other option what are the specific and concrete advantages am I likely to gain and at what cost am I likely to gain them? Stay with these two questions for each option for some time till you feel that you have enough clarity on the trade-off. This is one way to reduce the enamour of what we feel is the 'gut-level' option. Once this process is gone through with all the options, the last-man standing is the right answer.

Below each step is listed in order of criticality. Be sure to constantly remember that decision you make in the first step influences your outcome far more than the decision you make in the immediately subsequent step. That is, step 1 will influence outcome more than step 2. Step 2 more than step 3 and so on. So if your thinking time (or that of your financial adviser and planner) is limited, allocate it accordingly.

1. Intention / Objective --- Investment versus conscious or unconscious speculation

2. Time period over which money will be directed into equity schemes (equivalent to the sowing period for a farmer)

3. Withdrawal approach (equivalent to when and how the farmer will harvest his crop)

4. Amount to allocate (equivalent to the physical and psychological resources the farmer has at his disposal, including himself, his family members, bullock, farming skill, patience, past experience knowing that sometimes the rains are late and sometimes they are early, etc.)

5. Right fund house (equivalent to on who's land will the farmer plough on, from where will he procure his seeds, fertilizers, pesticides)

6a. Stick to tried and tested area of the market which in almost all cases will be large-capitalization stocks (akin to the farmer sticking to the age-old basics of farming and relying on his physical senses and common-sense, investing in machinery and technology selectively where it where he can clearly see guaranteed improvements in productivity without burning a hole in his pocket or further indebting him)

6b. Expand or narrow the market beyond what conventional wisdom would suggest (akin to the farmer trying out newer farming methods, genetically modified varieties of seeds, investing upfront in expensive machinery hoping for eventual pay-off over long-term from taking upfront risks).

Most should stop at step 6a. It is important to take a considered pause at this step and, do what Benjamin Graham would define as thorough analysis. All of us may not be endowed with the ablity that Graham had of analysing financial information of companies, or portfolios. None the less, research can imply taking a wide-raning survey of what well-known practitioners (as well as theoreticians) in the field of investment have to say. It is important to soak in as many view points as possible and not go simply by the suggestion of the financial planner or adviser, no matter how intelligent, or trustworthy she or he may be. This also applies equally to the fund house of your choice. Placing your trust in a fund house of repute is one thing but going blindly by their suggestion of specific schemes is quite another. Only you know your balance sheet, your future liabilities and your ability to withstand long periods of under-performance of your investments. Success in investment follows from four axiomatic qualities:Discipline, Patience, Common-sense and realizing the heavy responsibility you carry on your shoulder when making investment decisions, as very many of us are likely to investing on behalf of our loved ones.

While doing the wide survey, one will discover a series of view-points that appear to be highly similar and are touted to be 'conventional' wisdom. But actually, when thought over a bit more, they turn out to be just patterns of thinking that people have fallen into. There will be another series of considered judgments that will be highly analytical, rational, conservative and coming from the mouths of very experienced (and successful) practitioners. It is a characteristic inherent to views of such practitioners that their views may appear too short, too simplistic and too rigid in one sense. But these are worth paying very close attention to because of the very fact that they are simple could imply that, at bottom, they are reflecting the first principles of investing. However, it is very critical to really understand in what context a practitioner holds a certain view. For example, a low-cost S&P 500 Index Fund, is actually one of the best 'productive assets' in the US equity investment landscape today for the general population. From such an assertion it is wrong to conclude that Index investing holds true in all situations and circumstances. The composition of the index, the cost of construction and management of the index, and availability of definitively superior equity funds may weaken the argument for Index funds as far as their devastatingly superior mathematical advantage is concerned. Indeed, even in India, for a person with small amounts of money that has been earned through very hard-work, and which may mean a lot to that individual, an Index Fund is a definitively attractive proposition in the very long-term. Indeed, it may hold a lot of value for others too. But one should not invest in Index funds because the best practitioners have said so. One should invest because one clearly understands what an Index Fund is, where does it really derive its advantage from, and, importantly, the fact, that while it may not be the best option in all contexts, it is certainly a good de-facto option in many contexts.

The important point is this: focus on substance and not form. There is nothing magical (or more accurately, mystical) about the word 'Index investing' as there is nothing magical about the galaxy of words 'large-cap', 'blue-chip', 'mid-cap', 'small-cap', 'growth', 'value', 'dividend-yielding', 'emerging markets', 'balanced funds', etc. The prudent course of action is to erase all such tems and their associated classifications from mind and understand that at bottom all of these represent a 'set of securities'. To those who are willing to make the effort to source the diversity of view-points in the investment sector, digest and synthesize them, will come to the conclusion that there is no need to take sides. The important point is to form a rational opinion, and in the process of forming the opinion, test the increase or decrease in the level of conviction you have in that opinion.

But this conviction is not an article of faith. It has to be grounded in three very basic questions:

1. What is the cost of holding the selection of one's chosen group of funds to eternity? (This video from John C. Bogle, considered father of Index Investing, will go a long way in answering this question).

2. What is the value from a particular selection of funds? (Value will need to have two parts: in terms of absolute returns after deducting costs if held till the timeframe you have in mind + psychological value (chiefly related to the ability of the portfolio to reduce volalitiy if your temperament, time-frame and/or circumstances restrict you from withstanding it beyond a point)).

3. Is this the most cost-effective and tax-efficient combination that will enable one to extract Total Returns (Capital gains + Dividends) from a reasonably broad cross-section of market capitalization?

In some ways, the crux of step 6a is to be able to arrive at a satisfactory answer to question 3 above with a reasonable degree of statistical and psychological confidence. Till you are absolutely assured that you have cracked question 3, keep trying. Please note that step 3 is not about finding the most optimal portfolio that will generate highest risk-adjusted returns. This is simply not possible. Those who claim to know this answer have forecasting and predictive powers, which by definition no sensible human being has or claims to have. The question 3 is about ensuring that you have eliminated all possible options that seemed enticing at first glance, but on closer inspection turn out to be full of gaping holes. That is, the right answer is, to repeat the earlier phrase, the last-man standing. More specifically, after you have chosen a given fund house or two, it is that combination of equity fund schemes from that house (or houses) that is superior to all other combinations. A suggestive help: restrict yourself to one or at most two schemes. Only then comparing combinations will be humanly possible. With 3 schemes, comparison becomes too difficult, even if one uses qualitative parameters. With a solitary thing, you could know what all can go wrong and what all can go right. With two schemes, you could know a little bit less what all can go right with both schemes individually and collectively and vice-versa. Imagine doing this exercise with three schemes. Literally, it defies imagination. Effectively you are building a portfolio of your own. Which means, maybe, you should be starting a fund of your own if you believe you possess such skills of optimizing multi-variable equations.

It is critically imperative to repeat the last quote that appears at the beginning of the page for the benefit of those who may have missed it: "An investment is an operation which upon thorough analysis promises of safety of principal and a satisfatory return".

Which means that: most should stop at step 6a. Those who wish to move to step 6b should clearly acknowledge that they are not seeking satisfactory returns and are willing to compromise, even a little, the safety of principal in the hope (or in exceptional cases definitive knowledge) of incremental profits. Those taking these steps should thus clearly understand the principle of marginal economics. A day to day example should make it vividly clear. Conventional automotive engineering wisdom recommends driving a passenger vehicle at 80 kmph to optimize engine and fuel efficiency as well as passenger safety on the highway. Of course, if temperamentally you do not have the discipline to stick to 80 kmph on the highway, the above steps are not for you (market analogy: you are speculating under conviction or delusion). But lets say that you prefer to adhere to this driving principle but, at the same time, you are experienced and mature, and hence, flexible and not dogmatic. You are on a two-lane highway and keeping to the left lane. You see from a distance that a slow-moving heavy vehicle is in front of you in the same lane. You know that soon you will catch up with the vehicle and you will need to overtake it. At this point, you look in the rear-view mirror and see the field open. So with minimal to moderate acceleration you overtake the heavy vehicle.

Instead it may well happen that you look in the rear-view mirror and see some traffic on the right lane behind you approaching at a speed faster than the one at which you are driving. At this point you have two options: gradually slow-down and maintain a fixed distance from the heavy vehicle in front of you and allow the traffic on the right to overtake you. Alternatively, if you judge that the traffic behind is quite a distance away and your vehicle can respond quickly to your request for acceleration, you accelerate to 100 kmph and skilfully overtake the heavy vehicle and move back to the left lane in front of the heavy vehicle before the traffic on the right lane zooms past you.

This is making decisions in day to day life at the margin. All of us do it, but most of the times these decisions are ones of habit and not careful reflection. Either because we have experience at what we are doing or we are plain foolish. In stock markets, very few can claim to have skilled experience. So most of the times for individual investors marginal decisions will actually incline more towards foolishness. To avoid this, while constructing a portfolio of actively managed equity funds constantly probe yourself on the tangible benefits you are getting (exposure to segments of market that conventional large-cap/index schemes do not provide but which can improve your risk-adjusted returns over the time-frame you have in mind, orthogonality of the portfolio (i.e. improved risk-adjusted diversification), etc..?). Against this, ask yourself, what is the fixed expense in form of fund management fees will I incur? Do the benefits lend themselves to some kind of quantification? If yes, does the quantitative benefit outweigh the incremental management fees to be paid? If the quantitative benefits are not easy to arrive, then are there sound qualitative factors, or a high number of research efforts, that support the act of venturing into non-conventional areas of the market, including mid-cap and small-cap? If the answer a resounding yes then proceed.

However, in spite of such an exercise yielding a negative result or a weakly positive result, those who still insist on proceeding must acknowledge that they are, in the words of Roger Lowenstein, 'capitalizing hope'. It should be noted in the same breath that such an exercise is not to prove the superiority of step 6a over step 6b. It is to ensure that those who are planning to construct their own portfolio at least have an arguable rationale for the same. Note: An exercise of this nature should be run strictly in context of the decisions made at step 3 and 4, viz., period of time over which money will be invested and period of time over which money will be withdrawn from the equity funds.

Or, if you are programmer, you will be able to instinctively understand this point through remembering the dictum gleaned from the books of Donald Knuth: premature optimization is the root of all (programming) evil. It is important to first ensure that the program runs; and, only subsequently, that it runs consuming minimal quantum of time and space resources possible. No point having a super-efficient program doing everything complex beautifully but failing on basic functionality (those using a Windows system would perhaps nod their heads in agreement).

On the other hand, you do have complex systems that do the simple as well as the complicated stuff and look beautiful too: like a Macintosh. But they are just so expensive, and when something simple goes wrong, they make you feel so helpless (those having been a victim of an Apple-designed solution will perhaps nod their heads in agreement, hopefully with more vigour than the ones who have been at the receiving end of a problem in a Windows system). Because once a Mac fails, it is nudging you, saying in a very plaintive tone: please take me to an exclusive saloon and spa to redo me all over and make me look like my next-generation cousin that Apple has just launched. It of course fails to tell you that a visit to the saloon and spa (which is nothing but an Apple Store) will cost you a bomb. You are of course not stupid. You can see through all this. But it keeps goading you: to repair me will cost you a bomb in the long-run as my hardware and software is so beautifully and intricately integrated. Why not just buy a fancier, slicker and sexier version of me?. And you shake your head in despair: why, oh why, did you have to be so damn integrated? The device answers promptly, without batting a self-conscious (and guilty) eyelid: because that's what makes me so elegant, beautiful, slim, smooth, curvaceous and super-sexy. After all, didn't you buy me because I look and feel so sexy in the first place? There is a price you have to pay for being a sucker for beauty some day, don't you think? In love, as in war, what starts well, usually does not end well (American ground troops in Afghanistan would be able to vouch for it; so much so that they would repeat it with all the more vehemence even under a constitutional oath in a Senate hearing which is likely to make their bosses in the military and intelligence establishment look a little caught up with their pants down).

Moving from Step 6a to Step 6b is entering the domain of optimization and a danger zone involving forsaking what is simple, better guaranteed in the desire for what is complex, outwardly appealing and and, as a logical consequence, uncertain. What is more, there are so many sexy sounding equity schemes that they make this transition (From 6a to 6b) very convenient. However, they also ensure that you can never go back from 6b to 6a again without incurring heavy losses.

Buddha said: Ignorance is the root of all evil. Knuth blames it on pre-mature optimization. Both effectively are saying: tread with caution. The demands of both the wise men also imply: complexity demands discernment to simplify and profit from it. Discernment requires sustained effort to strengthen it. For those who possess the time, can and should try. For the rest, being constantly cautious is tiring after a while. So it is better to meet the demands of the two wise men through a simple home-made brew suggested by Ken Thompson: when in doubt, use brute force. Step 6a is this home-made brutish brew. It obviously comes with convenience (no need to move out of your bed and go to a doc) and cheap (it's home-made after all!) written all over it. Drink it and you shall be fine. You may not gain the strength of an athlete. But then you are not competing for the olympics. A morning jog is as far as your muscular movements (and ambitions) stretch. Note: Joggers who think themselves athletes are invited to participate in Mumbai Marathon.

However, if you know you are an athlete, or want to train to be one, move to step 6b.

Those joggers who run Mumbai Marathon may feel slighted. What we are saying is that those who should confine themselves to Step 6a have pre-maturely moved to Step 6b. So to raise their spirits, let us tell them: the fact that you have navigated successfully to Step 6a is more than a marathon. To go back to our earlier example of overtaking on the highway: let us say that you have accelerated from 80 to 100 kmph thinking the traffic in the right lane is quite behind, giving you enough time to overtake the vehicle in front of you. However, it may so happen that suddenly someone in that amorphous mass of traffic decides to speed-up while you are mid-way through your overtaking manoeuvre . If you are lucky to glance at your mirror, you will suddenly see this lone ranger approaching furiously in your rear-view mirror. What are your options? Difficult to say. It is quite likely you might reach a heavenly home instead of your earthly abode. If drivers can be like this, can't a market with million participants be as crazy? You need to enter the zone of investing in equity mutual funds with enough cash reserves at hand so that when confronted with the possibility of a pre-mature heavenly home, you keep calm and give yourself time to work through your next moves. That is why it pays to remember: decision arrived at in step 1 contributes far more than any other decision. Likewise, for steps 2, 3, 4, and 5.

Hope the Marathon runners are feeling vain all over again. To that hope we dare to pile up one more hope: this time their vanity shall actually be sound pride. Pride on not registering a single day of inattendance in their jogging schedule. And not the false pride that comes with training the whole year for that one day of Mumbai Marathon when you can show off to yourself and to those who care to listen about your disciplined year-long exertions for that one day. It kind of sounds silly now doesn't it when you look at it this way? Imagine what would your kid say about you when your misdemeanours in investing mis-fire revealing that in fact that they were outright speculations putting to shame a gambler in run-down underworld casino, all in the hope of making it big in that one big bull rally? Most of us do not think about it because it never strikes us that our kid could think of us in that fashion: especially when some of us are likely to fancy ourselves being million feet above the ground when such a profound doubt hits the mind of our child; while the more pragmatic ones know that they will be six feet under the ground. Meanwhile, the markets continue to exist on minimal ground(s) always seemingly moving from one existential crisis to another carrying the participants along with it: like the Pied Piper carried out all the rats of the otherwise peace-loving town.

But lets not be so biased. We must also remember that the Pied Piper also carried away children the first time around. It would be better to be part of the first round of outing with the Pied Piper (lets call it investing) than the second (lets call it speculation, or should it be the other way around?) --- no offence to the Pied Piper. He played his flute brilliantly like the markets do every day from morning to early evening. Thank God, they are closed in the night. Or are they?

Disclosure: The author has all his long-term investments in corporate debt and pure-play equity mutual funds routed through two fund houses. Furthermore, besides the National Pension System, he has majority of all his investments in equity concentrated in two actively managed mutual funds which diversify across a mix of investment styles and capitalization, divide emphasis equally between dividends and capital gains, have been in existence for at least 10 years and also provide a very limited exposure to emerging market stocks. His intended period of accumulation is 10 years and minimum intended holding period is 15 years (preferably 20 years). This constitutes, what the author terms the 'diversification block' of his exposure to the public stock market and is meant to complement his investments into the National Pension System (which he prefers to think of as his 'accumulation block').

In addition, the author had invested a material part of his balance-sheet during the COVID-induced market panic in March, 2020, in a large-cap and small-cap sscheme from the same fund-house. This one-time 'lump-sum' block was to provide for the lack of any equity investments in the decade past.

He would not recommend anyone else to follow this approach, unless they have studied and thoroughly eliminated all other option (and this two fund-house)s, and have been logically (and naturally) led to conclude that this method of investment suits their circumstances and temperament. Please note, there can be far superior approaches to garner returns than this approach even after adjusting for risk. However, the author's experience and competence allows him not to venture beyond the option he has chosen for himself.

P.IV.S Handling of gift monies (endowment)

See also: P.VI.S

Gifts received from family & kin, or share of income received from assets owned by them, should be accounted for separately. Such receipts are an heirloom and blessing in disguise and should be treated as such. They should not be consumed but counted upon to add protection to the remainder of one's balance-sheet as well as to increase security for the next generation. In financial and legal terms, such receipts are an endowment: something that 'endows' (enables) one to do something, hopefully good. How one deals with endowments can greatly influence the solvency of one's balance-sheet.

An endowment must be handled by rules and must be protected from the tax-man to the extent feasible (under law). Endowments are received erratically, must be rolled-over systematically, profited from incrementally, and deployed, when the times comes, all at once. This, in a nutshell, can be thought of as recycling of cash. Investing endowments is therefore far from easy because it is difficult to find instruments that can preserve the legacy and intention with which something was endowed as well as earn high returns while tax-efficiently recycling cash.

The suggested technique to deal with large endowments is as follows: put the entire, or majority of sum received into one or more sovereign-backed instruments. The interest earned on these instruments should in turn be ploughed into non-term life-insurance contracts. Subsequently, as these life-insurance contracts mature, the cash so received can in turn be invested in various other instruments, including common stock.

What happens if the above formula is allowed to run? Initially, the endowment so received is attached to something 'safe and assured'. As that safe instrument gives out some more cash, that cash in turn is used to further purchase protection (life-insurance contracts) to strongly secure the balance-sheet. By the time these instruments (the sovereign instruments and the life-insurance contracts), sufficient time has elapsed for the balance-sheet to further mature and fortify so that the same technique, or a variation of it, can be repeated.

Essentially, the original endowment received and further benefits derived from it are used to generate more benefits. This cycle can be repeated as many times as required (i.e. recycling of cash) thereby turning-over the original endowment many times, all the while providing adequate fortification. This method of handling endowments: fortifying the balance-sheet (solvency-protection): provides the family stability, safety and independence so that it as a unit can continue to grow and flourish and thereby fulfilling the real intent of any endowment from near and loved ones.

However, to execute upon this technique, it is important to understand better the role of life-insurance contracts. Most financial advisors tend to look down upon them but they play an important intermediation role in helping recycle cash properly.

Life-insurance contracts.

A typical life-insurance contract requires making regular premium payments for a certain number of years, after which the insurance company will repay part of the premium it collected, in instalments or all together, along with various kinds of bonuses. While this contract is in force, it provides a life-cover, the reason it is called a life-insurance contract.

Now, in absolute terms, the cash received from such a contract is likely to be only slightly more than what is put in. Further, the value of the cash received, i.e., its purchasing power will be at least 10-20% % lower than what was put in. Why? Because with time, inflation would have eaten away the strength of the currency itself. The life-insurance contract had no provision to protect against such erosion of value.

The question then is: what if the money was put into a simple recurring or fixed deposit and kept there for the same period of time? Quite likely, the deposit too would yield a similar result, i.e. the deposit will also likely lose its purchasing power to a similar degree over time. This is because what the life-insurance company or the bank can pay is largely governed by the expected general levels of interest rate in the economy, most represented by the rate available on a variety of government securities. Therefore, both these instruments cannot deviate too far from the general levels of interest rates and as a result, from the stand-point of returns, a life-insurance contract is very similar to after-tax returns on a fixed or recurring deposit of a similar tenure.

Then why not just use a fixed or recurring deposit instead of a life-insurance contract? Because of three reasons: behavioural, tax-related and life-cover. These contracts take in cash in a disciplined manner, lock it forcefully for a pre-defined period of time, while, simultaneously, making it easy to take out cash seamlessly in large chunks in a tax-free manner upon maturity - an under-appreciated benefit in an environment where the interest rates are low and likely to remain low. Further, these contracts offer a life-cover which promises to pay, in the event of death, at least the sum assured even if not all premium-payments were made.

The benefits of this last feature (life-cover) are often not accounted for and appreciated properly: on occassion of death, receipt large lump-sum amounts of cash eases many a financial stress and anxiety. It buys time for the family to deal with the loss in a graceful and mature way. It also fits well with the essence of any endowment: to provide a peace of mind and security to the family.

Of course, the life-cover benefit in isolation does not make a case for non-term life-insurance contract, for a term life-insurance contract provides a much greater cover at a fraction of the cost. But, when the benefit of a life-cover is placed along-side behavioural and tax-related advantages, a life-insurance contract makes a reasonable case for itself.

While the life-cover certainly makes a life-insurance contract better than a simple fixed or recurring deposit, but what if the endowment was invested instead in marketable securities, primarily the public stock market, wouldn't it protect the purchasing power of the endowment better?

There are two problems here: one of technique and another of time. Investing (committing) large sums of cash in a short-period of time in the market for financial securities requires a high degree of skill. It is possible to do so over a very extended period of time, but then it presents a problem of what to do with the cash in the meanwhile? Should one keep such large sums in a liquid fund, or a fixed deposit? What if there arises frequent temptations to spend some of it wastefully? The amount of management and mental discipline this demands is not easy. For almos everyone it is not advisable that they pursue this course with sums received as endowments as these endowments truly constitute a legacy.

The second challenge of time concerns the definition of long-term. In the long-run holding a claim on a productive business activity will certainly yield greater benefits than handing over the same cash to a bank or a life-insurance company. The problem lies in getting to the long-term. Any marketable security by its nature suffers from volatility, it goes up and down, sometimes viciously. In case of an event such as death (or any planned major event such as purchase of house) which requires cash immediately and in large doses, the public stock market cannot be counted upon to provide the security that fixed-value instrument can, especially an insurance contract.

Long-term then may demand waiting for a much longer period, that even say, the typical period of a life-insurance contract, to realise the full benefits of the original endowment. All this while, it could very well have been possible to recycle the endowment through a couple of cycles: it would have been possible to earn some interest, buy some protection and reinvest the proceeds further. Each person would prefer to see the principal value of his or her endowment remain constant, realise constant, visible and predictable benefits and buy himself or herself time to act more intelligently in the future.

Psychologically, then, the proposed scheme involving life-insurance contracts works out better, and in money-matters, when dealing with large sums of cash, psychology is more important than hard arithmetic. It may be acceptable to live with a 10-20% reduction in purchasing if it comes attached with surety and predictability, and a sense of greater control. It is this surety which provides a singular lens through which to view non-term life insurance: as a safe cash collateral on the balance-sheet with contractual guarantees. A collateral is something against which you can pledge something else. An instrument is acceptable in lieu of a pledge if it has surety, guarantee or iron-clad assurance or honour attached to it.

Non-term life insurance contracts then, like a public provident fund account, effectively house the honour of a family, against which the family or individuals within it, can pledge the purpose of their lives, i.e., make something good of their lives. This use of non-term life insurance as a self-contracted, self-owned, secured cash collateral is its singular merit and cash collaterals the best forms of reserve assets on the balance-sheet. Possession of a non-term life insurance contract and an ability to honour it (make regular premium payments) is then the best means to build strength of financial character.

That is not to say that the loss in purchasing power is to be ignored. Investments in marketable securities could certainly be considered once the initial endowment has been turned-over at once. It is possible then to make good on some of the loss in purchasing power when the life-insurance contract matures. At maturity, large proceeds will be realised, as well as some proceeds might be received before maturity (such as in money-back plans).

These proceeds (benefits) can be put into service as follows: to be set-aside/parked to meet and current future expenses. This allows two benefits: to avoid breaking other savings, in turn, allowing those investments to continue their compounding. At the same time, it allows more of current income to be directed into marketable securities that provide inflation protection. Together, these measures indirectly ensure that the inflation-protection strength of the balance remains unimpaired.

However, if these proceeds are not needed for consumption, then they can be used to set-up an even larger cash collateral through purchase of a larger non-term life insurance contract(s) with longer premium payment term(s) and the process can be continued indefinitely creating the best means possible of intergenerational transfer of wealth.

In summary, this method of handling large sums of cash by converting cash into safe, interest-earning and tax-efficient cash collaterals (with contractual guarantees) recycles cash, fortifies balance-sheet, and allows for an intergenerational transfer of capital when dealing with large sums of monies.

It is therefore easier to think of non-term/endowment-like life-insurance policies as handing over large sums of cash at once, or regularly, to an insurance company for safe-keeping for some time while other aspects of one's life take shape and settle down. These insurance companies by holding our cash in trust, and also providing life cover, provide a service which will be very difficult to design or piece together by hand.

These policies are a contract between oneself and the insurance company. The insurance company can keep its side of the bargain provided the other side keeps its. To fully realise the benefits of these policies it is therefore important that all their premiums be paid on time and they treated as equivalent to a loan drawn from a bank.

P.V.S: The following approach is suggested in integrating The National Pension System (NPS) into one's balance-sheet:

1. Open a NPS account as early as possible, preferably at the age of 18.

2. Set the initial mix of Tier 1 account as 75% (E): 12.5% (G): 12.5% (C)

3. Set the initial mix of Tier 2 account as 50% (E): 50% (G): 50% (C)

4. Decide how much to contribute in toto out of earned income to NPS and direct 80% of that to the Tier 1 account and 20% to the Tier 2 account.

5. Increase the total amount contributed to both the accounts by 3% each year, if possible.

6. Continue the contributions to both the accounts for as long as possible, preferably till the age of 60.

7. From the age of 40, reduce the equity component (E) of the Tier 1 account by 1.25% each year and divide it equally between C & G components. cContinue this rebalancing up till the age of 60. This ensures that over the course of 20 years nearly 25% (1.25% per year x 20 years) is moved (rebalancing) out of the (E) component to the C&G components to keep the ratio across the three asset classes at 50% (E): 25% (G): 25% (C) as required by the NPS Tier 1 account norms. This rebalancing is necessary as it reduces the volatility of the balance in the Tier 1 account as one approaches closer to the retirement age.

8. Upon turning the age of 60, opt to continue the Tier 1 account for as long as one's circumstances allow, or as long as the rules permit, which is typically 70 years at the time of this writing. Make no further contributions to the Tier 1 account. Every 3 years, reduce the equity component by 5% and divide it equally between the C & G components. This ensures that by the maximum permissible age of 70 (up till which the account can be kept operative), the ratio of equity in the total allocation will be around a third of the accumulated savings. This is sufficient to protect the balance in the Tier 1 account from severe disruptions or dislocations in the stock market when the entire amount becomes due for withdrawal at the age of 70.

9. Meanwhile, upon turning the age of 40, annually rebalance the Tier 2 account by increasing its equity component by 1.25 % each year and divide it equally between the C &G components. Continue this rebalancing up till the age of 60. This ensures that in the course of 20 years, nearly 25% (1.25 % per year x 20 years) is moved into the Equity component of the Tier 2 account bringing the ratio to 75% (E): 12.5%(C): 12.5%(G).

a. [Explanation This ensures that as the equity balance the Tier 1 account declines, it is off-set to some degree by the equity balance in the Tier 2 account. If the above strategy of contribution and rebalancing is followed diligently it ensures that the Tier 1 account balance, where the majority of savings lie within the NPS, is buffered from severe volatility or market disruptions. On the other hand, a smaller proportion of savings lie within the Tier 2 account, but their greater equity exposure provides an opportunity to benefit from any upside in the stock market in the years after the age of 60 before the savings are fully withdrawn from the NPS. On the other hand, even if there is a severe contraction in the stock market, since the stock-market is a much smaller proportion of total NPS savings, the overall effect on the total NPS balance can be contained.]

10. Upon turning the age of 60, stop contributions to the Tier 2 account and start making annual withdrawals of 5% of the accumulated balance. This is done for a simple reason: by the above design, the NPS Tier 2 account has higher exposure to the equity component. As a result, it is more exposed to wide fluctuations in the stock market. Therefore it is not prudent to withdraw the whole amount in a lump-sum mode. It is better to stagger the withdrawals over a period of say 7 to 10 years. These withdrawals can be carried out as transfer to the NPS Tier 1 account, or diverted to a conservative hybrid fund, or can serve as an important source of additional income. In the last case, it provides the comfort and space to delay withdrawals of NPS Tier 1 account as long as possible.

11. 70 is the outermost limit for deferring withdrawal of the NPS Tier 1 account. When the withdrawal is made and the Tier 1 account closed, whatever balance remains in the Tier 2 account must be fully redeemed.

12. Of the total amount withdrawn from the Tier 1 account, 60% or more may be received in a lump-sum manner tax-free and the balance is converted into an annuity. Thus, before making the withdrawal decision, it would be important to study the available annuity providers and again seek counsel to choose the right annuity product. The total amount withdrawn from the Tier 2 account, will be received as a lump-sum and the capital gains on this amount will be fully taxable.

13. In the case of the death of the contributor, the accumulated savings are transferred to the nominee (in this Spouse). There are three things to bear in mind on filing a withdrawal claim upon death: first, is the entire saving to be withdrawn as a lump-sum, or part of it used to purchase annuity; second, what are the implications of income-tax receipts of such funds in the hands of the nominee; and third, when is the right time to withdraw, shortly after death, or to wait for a while in case the stock market condition is unfavourable at the time of death. The rules of the NPS that govern these three conditions are periodically updated and it is important to study them before filing the death claim.

14. Finally, if at any time in future, there is a change in the rule that governs maximum age for closure/withdrawal of the Tier 1 account, or making purchase of annuity optional, it may still make sense to adhere broadly to the above set of guidelines, unless personal circumstances demand extending the date of withdrawal and/or taking the entire set of proceeds as lump-sum.

15. However, if there is a change in the rule which governs how the accumulated savings can be withdrawn: multiple times and indefinitely till the survivor is alive, then it is best to make annual or semi-annual withdrawals from the Tier 1 account. Furthermore, in such a scenario do not reduce the equity component of the Tier 1 account, below 50% in step 8. A healthy exposure to equity is necessary to make sure that the savings can last throughout the retirement.

P.VI.S: Note on handling large sums of cash: Circulation of cash vis-a-vis growth of cash.