|

|

|

|

Commenced: 26th September, 2023.

First draft: 12th November, 2023

Final draft: 10th November, 2024

Re-editing: 13th June, 2025

One person pretends to be rich, yet has nothing;

another pretends to be poor, yet has great wealth.

~~ Proverbs 13:7, The Bible

Key words and themes: Ownership of capital; Building a family corpus and legacy; Financing the family's future; Annuities and their import; The meaning of capital; The definition of a marketable security; Savings vis-a-vis investing; Warehousing of marketable securities; Being a banker unto oneself;

It is not the wont of the author to provide an index; but in view of the long and multi-part nature of this write-up, the following may survive for one:

Preface

Introduction

Being clear

A word on annuities

What is a marketable security?

The difference between saving and investing

Why save in the form of marketable securities?

Why the NPS: warehousing of marketable securities

Is the NPS tax-efficient?

Customising the NPS

Asset allocation

Customisability and volatility

Setting and rebalancing the asset-allocation with passing age

The Tier 2 account: 'investment' versus 'capitalisation' merit

Combining the PPF and the NPS: syncronising investment and capitalisation merit

Building a self-owned bank

Courage and creativity

NPS against (and with) Mutual Funds

Bringing it all together

P.S. Distortions of the market

Preface

When it comes to money, the prudent course of action for most individuals is to park their savings inside regulated and standard arrangements. In this regard, Indians are a fortunate lot as they can avail of two off-the-shelf ready-to-cook products called the Public Provident Fund (PPF) and The National Pension System (NPS) open to the general public since May 2009. In addition, there is an important role for the much derided (and more often than not, wrongly sold) non-term life-insurance policies, provided the policies are simple and straightforward, without too many bells and whistles attached, and are purchased at the right time through the right channels.

Yet, time and again, individuals are tempted by the esoteric, the novel, and the popular. The constant desire to act and move money around without rhyme and reason results in an avoidable inevitability: inspite of earning much many fail to let their money make a material difference to the quality of the choices they make through the remainder of their adult lives. More money then only lands up in engendering more hassles.

While this primer centres on the NPS it does so from an overarching personal finance architecture outlined here. Being a product of many moving parts, the NPS affords an excellent opportunity to use its service to bring out some principles of life-long importance that underlie that architecture. Thus, even though this primer starts from the NPS, it ends up on a very different note: the idea of being a 'banker unto oneself'.

It is a powerful idea that can cut both ways, and hence not meant for everyone. It is likely to appeal to those who love getting under the skin of their money-management, which, in turn, involves familiarity with the basics of accounting and book-keeping, an interest in keeping abreast of regulatory changes and finding that time everyday to curate their balance-sheet. They shall be able to fully appreciate and implement it. The casual reader advisedly should not blindly apply what is stated hereunder.

Still, this primer has something to offer even to the latter: an intuitive grasp of the NPS along side some interesting terminologies and concepts in finance. Self-education, after all, is never in vain, and it is in that spirit that it be held that this primer is not financial advise but a financial perspective and an education based thereon. It is not an instruction manual with a ready supply of answers, instead it busies itself with concepts, use-cases, and examples — all in aid of building a system of thinking about deploying hard-earned savings.

But while this primer eschews the specific, it is nonetheless detailed, explicit and repetitive to drive home key concepts. Such repetition will prove valuable for this primer's primary audience: those not earning high income but who still take pride in handling their money responsibly. Their lack of financial training hardly deters them from discharging their responsibility, since they are those who wish to create an inter-generational family nest-egg. For,

A good man leaves an inheritance for his children's children,

but a sinner's wealth is stored up for the righteous.

~~ Proverbs 13:22, The Bible

Details and repetition help such individuals to bring common financial terms into their daily family conversations. It may also be noted that instruments like the PPF and the NPS are subject to regulatory changes from time to time, and while every effort may be made to keep this primer updated there is no guarantee that some regulatory change has not overtaken this primer. Hence, the reader is strongly cautioned to cross-check and verify the regulatory aspects stated hereunder directly from the concerned website of The NPS Trust.

In the ultimate analysis, though, there is no known substitute for paper-and-pen ready-at-hand when it comes to savings, financing, and investing. Concepts that that dot these domains demand that they be worked out by hands – several times sometimes – before they choose to partake of their utility. This is because entirety of this conceptual armoury is really fabricated inside factories of arithmetic and accounts, not the most popular of joints for entertaining heart's desires. They prefer instead to be supervised strictly by conventions and rules, a strictness best learnt by following it faithfully. It is thus only the duet of pen-and-paper best inscribes their rules onto the mind; and once firmly imprinted it remains an uphill battle to dislodge them – much to the chagrin of those around.

(N.B. The reader will more than a few times find this primer punctuated by text in brackets such as this, beginning with N.B. in italics. He may skip over it on first reading without significant loss of meaning; but inside of them attempts are made to showcase first principels that may have no direct bearing with the subject matter-at-hand.

For, while savings, finance, and investing is about money, money itself cannot be spoken of without reference to the principles that govern how men live. It is for this reason that quotes from The Qur'an and The Bible are suitably interspersed as in their brevity they compress more truths about financial wisdom than what the textbooks of finance struggle to get across. For, without exception, it is ultimately wisdom which is marinated that gives feet to knowledge.)

Those curious for sources that sparked building blocks of this primer, may make note of the following books, publications and sundry online material. (These are in addition to those listed at the link given above.)

1. "Security Analysis" by Benjamin Graham and David Dodd (Seventh Edition).

2. The letters of the Chairman to the shareholders of Berkshire Hathaway.

3. The Merriman Financial Education Foundation.

4. "The Infinite Banking Concept" by Nelson R. Nash (Fifth edition).

5. "A Safety-First approach to Retirement" by Wade Pfau (2019).

6. "In defense of annuities: from accumulation to decumulation" by Moshe A. Milevsky (2021).

7. The mechanics of money as it exists today, as covered through the library of videos housed at the "Eurodollar University" channel on YouTube.

8. Michael W. Green, who is able to bring an integrated approach to thinking about finance, i.e. piecing together variables from real economy with financial ones to forge a narrative which intuitive thinking can absorb. His writings are accessible at his Substack.

9. The nuances of practising 'privatized banking' as outlined in point #4 (above) at the level of a family / family-business at "The Money Advantage Podcast" channel on YouTube.

If the diligent reader wishes to pick up only one of the above for lack of time then the recommendation is to pick #4, i.e., "The Infinite Banking Concept" by Nelson R. Nash. It is bound to change what the mind makes of money.

Introduction.

To begin a consideration of the NPS is to start from the idea of accumulation: the notion of taking a portion out of a family's monthly savings kitty and putting it aside undisturbed so that it builds up over a period of a generation – twenty to twenty-five years – thereby accumulating a sizeable corpus. It is important to note that accumulation is carving out a small yet vital portion of the total savings and not appropriating entirety of it.

The purpose of such a family-corpus is to meet known expenses of the future when other sources of income are likely to prove inadequate. For long, life-insurance policies were used in service of this end, and they still can and do; but today along-side them, it is also possible to use the idea of warehousing marketable securities.

The inclusion of marketable securities though is governed by the time-to-the-future when the services of such a corpus may be called upon. If such time beckons at some distance then it offers the possibility to divert a reasonable portion of family-savings to marketable securities, i.e., stocks and bonds. The mechanism of the NPS is a convenient means to do so for the vast majority of lower and middle-class urban Indian families.

Though the term family may seem quaint its use is not without reason. For, neither the terms individual nor household quite fit the charter, since in choosing to contract long-term financial arrangements lies the act of stewarding money. This act demands a purpose.

That purpose can scarce draw from the wells of "fulfilling one's passion" or "to exercise the ghosts of YOLO", as such desires not only suffer from superfluity but do not befit the sacrifices that instruments with a very long lock-in such as the NPS demand. Money, it may be said without hesitation, is governed but by a single purpose: to give tomorrow a chance to raise itself upon the good graces of today.

Family, then, is the smallest and the most versatile as well as adaptable of social units tasked with this charge, since values,, which form the soil of civilisational continuity, cannot gain hold outside the confines of a family or a family-like set-up. The act of stewarding money effectively reveals the convergence, or lack thereof, of the value system of any family in its entirety.

This stewardship, or more properly, accountability towards money represents the singular test of how the present has behaved with regard to the past and what is it going to direct to the future. The attitudes and actions inculcated with regard to money are what end-up joining or breaking apart at least three generations. By this account, money in its essence then is an ability to lay claim on the material resources of today so that we sustain and further ourselves in the right manner tomorrow.

And when We said: "Enter this city, and eat freely of it wheresoever you will. And enter the gate in submission, and say: 'A mitigation! We will forgive you your offences, and will increase the doers of good."

Then those who did wrong changed the saying to other than what was said to them, so We sent down a scourge from the sky upon those who did wrong because they were perfidious.

~~ 2:58-59, The Qur'an

This notion of being intentional about money and holding our relationship with it to account over long periods of time suits the idea of marketable securities, since in shorter time-frames all long-term marketable securities are afflicted with unpredictable changes in their prices. For them to verily fulfil the purpose implied by their name ('a security"), they necessarily demand longer holding periods, an inconvenient but incontrovertible fact.

This idea of a holding period is more properly labelled as time-preference in the field of economics and is informed by tradition wherein the notion of wealth was primarily confined to productive tangible objects including agricultural land, forest land, cattles, and physical metals amongst others. All of these, without exception, demanded that their owner handled them responsibly for long for them to be of proper use to their master.

Forests harvested for a particular kind of wood, for instance, did not grow in a matter of a year, 5 years, or 10 years, as it took at least one generation to cultivate a forest area for the next generation to reap its rewards. Thus, in times past when their own lives taught men how to live this idea of very low time-preferences, i.e., long holding periods, was intuitive and integral to predecessors of modern and post-modern minds. This is not nostalgia but a reality observable even today in the workings of those who remain close to the earth to earn their living, be it a farmer or a miner.

Today, though, when wealth is overwhelmingly has come to be shackled to tradeable claims on activities of others through financial contracts, i.e. marketable securities, the notion of low time-preference has almost been erased from intuition leading, in turn, to genuine financial ignorance. This ignorance, though, is no excuse for the law that matching family-needs with nature of the underlying financial contracts lies at the heart of any family financial plan, and financing in general. For, every family is in effect not an investor but a financier of its own future, notwithstanding the propaganda surrounding the cult of 'investing in markets and remaining invested at all times for all needs'.

It is a cult which has all but succeeded in making a speculator out of an average saver, as someone who is attracted by and attached to movements of prices of financial contracts, rather than what the contract itself promises to supply over a tiringly long period of time. In all of the ever-effervescent pseudo-talk of investing, it is this very attitude to investing which is most notable by its absence.

It is surprising – or perhaps not – to see people exhilarate at rising prices while commiserate at falling ones. To not participate in the chase of rising prices is certainly difficult, since the alternative is even more difficult: to carry the reminder that those who chase rising prices will at some later stage get trapped in the whirlwind of falling ones. Cliched reminders such as these are easily cast aside in an age when the edges of forgetfulness are lubricated aplenty by the craving for more money as well as the envy of the neighbour inherent in every soul.

Against such a backdrop, the NPS, as will be seen, is an instrument to help families lay claim to the idea of investing, that of reallocating their savings to long-term financial contracts, in the proper sense of the term, provided they invest to finance their future needs. What follows therefore is geared for those who grasp this axiom.

Say a family were indeed to hold such an attitude then how much of a corpus ought it accumulate? The fact of the matter, however inconvenient it be, remains that the answer to this quandry depends on every family's collective income earning potential, the weight of its own past decisions, and the degree of luck it enjoys in relation to sound physical and mental health. However, what is always within a family's reach is the system-of-values it adopts with regard to where and how it chooses to source its income and spend it. Wisdom tellingly commands that income earned righteously and upon which taxes are paid honestly is more likely to be spent wisely, and the resultant savings retained longer than otherwise would be the case.

It further pays to never forget that there are always four forces that are bound to work against any such long-term savings plan: costs, taxes, inflation, and callousness of the self. The NPS is designed as a one-stop shop to counteract each of them. Along with the Public Provident Fund (PPF), it is one of the most well-designed savings scheme available for securing long-term savings. In the likeness of PPF, it is a highly regulated and low-cost scheme with attractive tax-exemptions and set rules for contributions and withdrawals.

Being clear.

While the nomenclature of NPS while has the term 'pension' within it, NPS itself does not provide or guarantee a pension. In technical terms, the NPS is strictly a defined-contribution plan and not a defined-benefit plan, or, as the NPS website labels itself: a market-linked voluntary contribution scheme. Furthermore, it is also not a wealth-building tool whereby the sheer act of putting money into the NPS is no guarantee that that pot of money will grow at a fast clip.

What NPS is, however, is a mechanism to accumulate small sums consistently over several decades, after which a whole or a part of the savings thus accumulated may be converted to some form of a guranteed source of income to meet core household expenses, preferably through the use of annuities. It is thus best to think of the NPS as warehousing marketable securities to then sell (liquidate) them in an orderly fashion in order to provide a minimal level of income support at some point in a family's life. Though a mouthful, it is as close to a definition as is possible.

A word on annuities.

Annuities call for attention as the rules of the NPS mandate that a portion of the corpus gathered under it be compulsorily converted to annuities. Thus, before committing family-savings to the NPS, it is important to reflect on what an annuity really is.

(N.B. The proposition of compulsory annuitisation is not an unsound one, even though it be a restraining one. Behavioural restraint is something which has not endeared itself to modernity, especially the version of it which comes dressed in the neoliberal garb.

Under this zeitgeist, notions such as annuities will always be construed as a thorn under the hasty feet of a generation indiscrimantely peddled the addiction of instant gratification. It is an uncomfortable fact that presently such a generation constitutes a critical 'customer-base' for a lucrative portion of the financial industry, inflicting upon the clause of compulsory annuitisation a precarious existence. This clause is particularly susceptible to being rescinded under influence from that corner of the industry whose pay-checks depend upon continuously expanding its "assets under management".

Be that it may, it behooves not that a responsible family fall prey to such shenanigans; instead it commit to working under a self-imposed stricture that a certain portion of the NPS corpus has to be compulsorily converted to annuities, whether or not regulations stipulate it. As any prudent saver will inevitably come to realise that restrictions are, on the whole, helpful rather than harmful. But since most learn the lesson too late in life, be not amongst those who regret.)

An annuity is a simple transfer-of-risk insurance contract: a lump sum is handed over to an insurance provider who, in return, agrees to take on the risk to provide guaranteed income for the remaining life of the insured (also called the annuitant). An annuity contract is in effect a tool to partition any lump sum across time in a hassle-free manner so that it can last for as long as possible, a fact formally labelled longevity risk. An annuity is thus an insurance against outliving your means in old age.

In practice, this simple arrangement varies due to the ability to tweak certain features of an annuity contract: in particular, whether to take the annuity singly or jointly with a spouse; whether to start the income support right away or after deferring it for a few years; whether to give the entire lump sum, once and for all, to the insurance provider, or to demand some or all of it back upon death; and whether the support is required for the rest of the life, or for a fixed term.

An annuity may appear an outdated notion in a financial environment where interest rates are high which, in turn, breeds a misplaced conviction in a family's ability to make a corpus withstand the test of time. Such conviction, though, is laid bare during prolonged periods of low interest rates, followed by their turbulent upheavels. These times then spurn a belated realisation that individual smartness is shamefully inadequate to cover the risk of establishing a life-long guaranteed income-floor, and that only the concept of risk-pooling executed by quality insurance providers can (assure that floor).

(N.B. The fact that annuities are the oldest form of income longevity-protection, pre-dating the beginning of the Christian Era, should say something of their maturity as a 'product class'. It is also one of the oldest known forms through which the Sovereign borrowed from the public, such as the instance of the French and the English Governments fought one of their most pivotal battles at the turn of the 19th century by borrowing from their citizens through issuing annuities.)

Inevitably, as societies reach a level of mature organisation and a degree of cumulative material prosperity, non-term life insurance in general and, annuities in particular, become increasingly important. But to accept annuities requires refraining the mind from subjecting every financial contract to the mechanical arithmetic exercise of 'rate of return'.

In general, an appreciation of more complex financial contracts requires a level of emotional maturity which allows the intellect to discriminate between a piece of tradeable and dematerialised electronic contract compressed into a numerical blip on a flashing screen, as opposed to a contractual and legally-binding commitment. A sign of such maturity is the growing conviction that the need for insurance far outweights that of investment with the passage of time and age. (And no, term-life insurance is not the all-encompassing cure it is made out to be but is only one amongst many others in the swiss-army knife of insurance.)

In the previous section, the intent behind the NPS was defined as "It is best therefore to think of the NPS as warehousing marketable securities to then sell (liquidate) them in an orderly fashion in order to provide a minimal level of income support at some point in a family's life". The existence of annuity contracts now allows for the second-half of this definition to be thus rephrased: "... to then sell (liquidate) them in an orderly fashion in order to transform them into an annuity-ladder so as to establish and maintain a guaranteed minimum life-long floor on family-income".

This idea of an annuity-ladder is then the conceptual bridge which converts the NPS, from what is essentially a cost-effective storage-place for marketable securities, into a provider of income security. The present regulatory mandate of compulsory annuitisation effectively makes the NPS less of an investment vehicle, instead imparting it more of an insurance character. The hope is that this fundamental character of the scheme is not impaired since it is a wholesome product to fulfil a wholesome need.

What is a marketable security?

A security is a type of contract, i.e. a legal agreement, which sets out the terms under which capital is invested with an expectation to earn profit. It (a security) is a promise, as opposed to say a non-term life insurance contract which is a guarantee. This difference is not merely technical: it is the difference between having something in hand right now versus a promise of being given something tomorrow.

The word capital refers to that portion of any set of possessions which ranks front & centre. Capital need not always reference money as it may refer to skills, time, or some other valuable but latent productive capacity. Specifically, when it comes to finance, capital refers to the monetary ability, or in other words the strength of balance-sheet, to take calculated risks with an expectation to earn profit. As a corollary: capital is created when money is managed in a manner to develop such a balance-sheet capacity.

(N.B. By extension, a capitalist is he who happens to be in possession of such capacity, and capitalism is that system of social organisation which then allows such capacity that be available with different individuals to be pooled together in an arrangement mutually beneficial to its owners and the society at large. This of course sounds noble in theory; practice, as is its wont, reveals behaviour much at variance with theory.)

(N.B. A possession is called front & centre, or has capital value, if it is devoid of any encumbranches – money that is detached of debt, or skills detached of ill-health – while being available in surplus to expend, and which also makes itself amenable to practical deployment with a view to derive benefits for self and society therefrom.

Take, for instance, the case of non-agricultural land: it cannot be labelled capital if it cannot be deployed for residential, commercial, or industrial use due to, say, regulatory restrictions or geological peculiarities. If it can be, then it has capital value.

Likewise, consider a child prodigy: if the child suffers from psychological scars due to bad parental upbringing, its genuis remains on paper failing to constitute the family's capital.)

The term investment comes from the Latin term investire and it traditionally meant to cover oneself in clothes, and as applied to the field of finance, it conveys the meaning of giving capital a new form of dressing. Thus, investing capital means giving that portion of possessions which is front & centre a new form by tying it to a productive economic enterprise so that that capital may be expected to earn a reasonable profit.

In light of the above definitions then, a security can be understood as a particular regulatory arrangement which, under contract law, gives legal recognition, sanction and protection to this action of 'investing capital'. A marketable security, by extension, is that contract which can be traded on regulated public markets or through partly-regulated or unregulated over-the-counter (OTC) markets.

It may then be asked that how is it possible to trade a contract which is nought but a piece of paper containing terms and conditions which cumulatively govern how a certain sum of capital may be invested? The answer lies in recognising that even if a security contract is a product of a legal convention, it can nonetheless be priced; and it can be priced because it can be valued probabilistically, that is with a reasonable degree of assurance.

Now, the publicly-traded securities most accessible to a family are those which lay-down claims of ownership (or, in sea-faring terms, drop anchor) upon some portion of the balance-sheet of a corporeal undertaking.

Such claims, in turn, are of two types. The first is the one which grants a right to earn some form of regular interest with a promise of return of principal at some point in the future, and the second is a right to take a share of the total profit remaining after payment of all expenses, interest and taxes. The former claims are often referred to as fixed-income securities, or more popularly as notes or bonds; and the latter, stock securities, or stocks, or more popularly, and oddly enough, as equities.

It should never be forgotten that behind these legal claims lie actual assets. In finance, something is an asset if it is expected to deliver a stream of future benefits to those who have established their claims upon it.

Thus, marketable securities, of the kinds that the NPS provides access to, are contractual claims (either in interest or stock-form) upon assets of publicly-listed corporations and finances of State and Union government, so as to establish a reasonably strong possibility to earn and accumulate a continuous stream of income over time.

Now, these securities (or claims) can be valued because it is possible, as Benjamin Graham elaborated eloquently almost a century back, to arrive at an intelligent estimate of this income-generation potential of theirs. What is possible to value numerically can, by definition, be priced.

Now, this proposition holds easily for securities of entities in the public domain, including the government, if for nothing else than the regulations which govern such entities. These regulations compliances and disclosures which force these entities to routinely share information with its security owners. It is this act of disclosure which makes these securities marketable as it places their information in the hands of a greater number of interested parties who have every incentive to appraise their value from time to time. This involvement of a critical mass of self-interested parties endows these securities with an ability to be bought and sold (trade them) through regulated open-markets, such as a stock-exchange.

(N.B. While it is true that there is frenetic trading of these security contracts which happens on a public exchange, there is still a price-to-value equation that governs such trading. It is possible indeed for a prudent man to say whether the price is out of line with the value and not buy something because it is too dear in relation to its value.)

The journey, thus, from 'capital' to a 'marketable security' is a conceptually involved one, and it is a journey many have forgotten due to the denegration of that societal institution called the 'stock-market' into an open-for-all gambling den. Revisiting the conceptual engineering behind these common terms may help refresh remembrance and respect for the institutional aspect that underlies these terms.

The difference between saving and investing

No term perhaps gets bandied more carelessly than profit: it is deserving of more attention than the scraps (of attention) thrown at it. One reason for its lax use by the tongue is that its accounting identity could not be simpler: revenue less expenses. But an accounting identity does not a definition make; instead, a definition is that which provides a key to unlock its meaning.

A gentleman might correctly say that the term profit represents benefits accrued over a time-frame after all the costs, without exception and exclusion, have been honestly accounted for. A slight turn of the language and the term profit is removed from the clutches of money! It may now be said that while profit may be measured, or more correctly accounted for, in terms of money, it itself is not money.

For, all benefits, by definition, accrue when capital is put to work, or invested. What is therefore invested is capital and not money. This distinction is akin to that between the heaven and the earth: ignoring it will not make for a fruitful living.

To recap then, money is a unit of account (and medium of exchange) and not the unit of capital, and least of all a unit of investment. Money, when managed properly, constitutes capital, and capital when actively and systematically handled constitutes investment. Investments may result in benefits and those benefits, in turn, are measured back in money.

This confusion (between money and capital) is common because typically everyone sees what goes in as money and what comes out as money and, in the process, a unit of account is construed as a unit of well nigh everything else.

(Much as the reality of the distance between two points is independent of the unit of its measure, so is the quantum of real capital at one's disposal is independent of the unit in which they are accounted for.)

And it is this real capital, a family's real set of endowments, that is available with every family is what truly matters. It is also that which every family actually invests. And, without exception, every family is given enough to make what it will of it. For,

Have they not considered the birds made subject

in the air of the sky? There holds them only God; in that are proofs

for people who believe.

~~ 16:39, The Qur'an

When a family invests its real capital, i.e., it puts its endowments to work, it accrues real benefits. While some of these benefits are accounted for in money-terms, many others remain intangible and hard to account. Those accounted for in money-terms represent quantification, or monetisation, of capital through investing. But those (benefits) that cannot be (accounted for in money-terms) are still real even though intangible.

Thus, the result of a family investing its capital is accrual of current as well as future benefits, both tangible and intangible. A portion of current tangible benefits may be realised in money-terms and thereby may be said to constitute the savings of the family as the term is commonly understood.

(N.B. The watchful reader would have realised that a critical, if not the majority, of the benefits that a family receives are tacit, unmeasurable and unseen. Yet, modernity has trained the mind to value and chase only the seen ignoring thereby the much larger value embedded in the unseen. For,

And with Him are the keys of the Unseen; and none

knows them but He and He knows what is in the land and

the sea; and not a leaf falls but He knows it; nor is there a

grain in the darknesses of the earth, and nothing moist or dry,

but it is in a clear writ.

~~ 6:59, The Qur'an)

Now, when the family 'appropriates' these savings and houses it under the protection of certain vehicles: be it a bank deposit, PPF account, life-insurance policy, mutual fund scheme, or the NPS: it is more properly storing its savings, not investing.. Over time, as these savings grow in value, they constitute the monetary capital of the family.

In summary, then, starting with its initial endowments the family has managed to monetise them, thereby giving itself an additional form of capital (monetary). The common-error of thinking, at this stage, is to start believing that just because there is money at hand, the act of putting it to work is an act of investing. It is critical that every family cleanse itself of this notion at the earliest possible.

A family is not an investor of money but always, and forever, a saver of its monetary savings, unless it chooses to actively engage in allocation of its savings in earnest by acquiring the skill of investing monetary capital. Very few (families) either have the time or the ability to do so, and instead, what they really invest is their real capital, i.e., their God-given endowments.

For a majority of families therefore instruments like the NPS, even though they deploy savings in marketable securities, should be considered as means of safeguarding savings. It is foolhardy to presume that the sheer dint of taking exposure to marketable securities is an act of investing; rather, if the family saves its money intelligently, it may then be able to actually invest its other forms of capital more effectively.

Why save in the form of marketable securities?

Now, if at the end of the day all that marketable securities are nought but contractual ownership on a promised income-stream, unlike contractual guarantees embedded in a life-insurance contract, then it is but natural to question that does affixing monetary savings to promises – however much they be legally sanctified – constitute an act of intelligence? If so, why?

It is a fair question with no fair answer. For, while governments have always occupied the place of an important societal institution, whether one likes it or not, today public corporations have sinewed their way into how societies operate. A material portion of money increasingly moves under their ever-covetous eyes, and it is through them indeed that individual constituents of society have come increasingly to interact with each other.

There is no doubt that a promise (on corporeal claims) implies that the end result will likely differ from initial expectations: with a family landing up with noticeably more or less. But then the same argument holds true of other life-long important responsibilities: marriage, earning a living, raising a family, or enjoying good health. In coping with these responsibilities every family takes upon itself a measure of risk while trying best to protect itself against gross errors. It is thus hard to imagine that the responsibility of money-management may find for itself a different way than that which governs all other facets of life.

Nonetheless it is true that the risk which untolerably attaches to money boils down to not having it in adequate supply when it is truly needed. For, though today may not call into service the savings ear-marked for tomorrow, rest assured that that tomorrow is always waiting at the corner bend. And the steady passage of time guarantees that many such corner bends are bound to be encountered.

Now, in order to satiate this (need of timely and adequate supply of money), it is commanded (that) a family stitch together a motley collection of guarantees in the form of long-term life-insurance contracts – preferably permanent whole-life or some variant thereof – with an intelligent speculation on the future through collecting claims of ownership on engines that own a critical mass of society's capacity to produce goods and services. It is through this combination that savings are capitalised, i.e., transformed into a base of monetary capital.

And it is only within such an assemblage that marketable securities have a capital role to play and never outside of it. Indeed, never has this role been more pronounced in mankind's history than today and that is due to a phenomenon which has vividly stamped its authority over the viscera of societies of the few centuries past, much to the delight of the Merchants and the regret of the Lords.

On one side of this phenomenon lies the unrelenting advance in the science of material engineering to harness the potential energy inside every molecule that nature has to offer, with ever and ever greater efficiency. And on its other side lies hidden the murky trail-of-transformation of money from that singed to noble metals to one composed of only circulating credit in the form of bank IOUs (lit. I Owe You) minted gleefully with an ever-increasing carnal appetite.

Money and energy, a moment's reflection will serve to show, have never been one apart from the other; joined, instead, very much at the hip so that changes in one flow over to the other side in lock-step. Their relationship constitutes, in the systems-thinking language of today, a dynamic. And it is this defining dynamic around which modern society continues to organise itself.

Its most recent manifestation reveals itself as an abundance of energy financed with debt held on the balance-sheets of private banking channels and the Sovereign, debt that the ordinary saver naively believes to be his hard-earned savings. It makes for strange times indeed to try to seek an honourable survival whilst this dynamic continues its march face forward, showing little signs of abating, and with no precedence to bank upon. There is no parallel in recorded history to match the scale and intensity of what has happened on the planet in the past two hundred years.

The difficulty (for the ordinary family) is further compounded by the ingrained ignorance regarding this dynamic amongst those who bake their bread teaching economics and happen to occupy high-chairs at important public posts, who, in turn, produce an equally clueless army of pupils who then go on to glibly manage the hard-earned savings of others. When the doctors aren't properly trained to diagnose, how trustworthy is the medication administered to the patient?

At first sight it seems a mystery for sure that a group of individuals, who otherwise have the intellectual equipment to solve complex algebraic formulations, fail to grasp the presence and gravity of such a potent dynamic. The answer for all of recorded history has always been the same: when you serve men an opiate they present themselves as able and willing to get addicted and to commit to remember less whilst forgetting much.

Another simple question has also always sufficed to identify the opiate pervasive in the modern era: what does the mass of mankind worship today? The answer, as they say, is blowing in the wind. The skill that mankind has mastered with reference to the money-energy dynamic compels that mankind necessarily create a new world-wide cult called efficiency. (Modern lips may haughtily smile when their eyes read of the fertility cults of yore in history textbooks since the modern man prides himself much on his logos and not so much on his eros.

Yet, it is hard to comprehend how the incessant pursuit of efficiency remains any distant apart from worshipping the "cult of fertility". For that matter, the requisite ritual edifice is very much in place as this self-invented goddess of efficiency may only be pleased by a continual sacrificial offering of "GDP growth" at her altar. The spectre of deflation haunts her, a bit of inflation greases her, while a lot of inflation inflames her.

And fabricating this "growth" in order to please the goddess requires an unrelenting cranking up of the lever-of-leverage through creation of more and more of bank IOUs out of thin air so that a majority of men consume in abundance today what they would otherwise have left as legacy for their posterity to prosper upon. The fact that all of this is carried in the name of progress makes the whole show a preposterous farce.) All in all, efficient in production and consumption for sure, but to what end and at what cost?

(N.B. This self-reinforcing money-energy dynamic and its accompanying cultic idol-worshipping culture has without doubt led to a rapid expansion of and access to untold material production. But it is an inescapable law of action that as one set of dynamic expands, it must automatically be matched by the wilting into the willows of another; and in this particular case, it begins with the visible decline of other, more intangible, forms of truer societal capital. The overall resultant may more properly be labelled a Faustian bargain.

And it is a bargain whose knowledge no longer remains confined to hushed voices inside private chambers; indeed it circulates as an open-secret amongst those with some critical ability to raise the right questions. The unflowering of this virgin secret, so zealously guarded by a section of the wheelers and dealers of money and ignored by the intelligenstia, makes it increasingly plain that chasing the deity of efficiency has caused irrevocable harm to beneficial forms of co-existence, with the notion of family being the first in line of shooting.

This fissuring of family has been achieved through the corrosive and continuous chipping away of the idea of individual and collective moral responsibility. And a collapsing family structure draws within its destructive fold the palpable loss of heritage, traditions and variety in cultures. For, the double-edged knife of shame and regret that restrain the appetite has been dealt a body blow. For,

O children of Adam: We have sent down upon you raiment

to hide your shame, and as adornment; but the raiment of

prudent fear, that is the best. That is among the proofs of God,

that they might take heed.

~~ 7:26, The Qur'an

O children of Adam: let not the satan subject you to means

of denial as he turned your parents out of the garden,

removing from them their raiment, that he might make

manifest their shame to them. He and his kind see you

from where you see them not. We have made the satans

allies of those who do not believe.

~~ 7:27

O children of Adam: take your adornment at every place of

worship; and eat and drink, but commit not excess; God

loves not the committers of excess.

~~ 7:31

And every man: We have attached his fate to his neck; and

We will bring forth for him on the Day of Resurrection a writ

which he will find unrolled:

"Read thou thy writ! Thy soul this day suffices as reckoner

against thee."

~~ 17:13-14

Seclusion, the last refuge for the frayed soul, too no longer remains an option, for, that levity of material abundance has certainly come at the cost of significant, and in many ways, irreplaceable degradation and deprevation of otherwise prime and pristine commons.

But ultimately, where this bargain burns the stomach most is when high-voltage material inequality meets the sight of the last remnants of power flocking towards fewer and fewer societal stations deploying means deceptive, devious, perfidious, and perverse. In other words, one set of power-broking elites replaced by only power-brokers of the crass, uncouth and bigoted variety.)

The net effect is a society bed-ridden with sharp, sudden, discontinuous and unpredictable twists and turns. An ordinary family, unwilling to forsake its moral compass in the midst of this madness, is surely bound to be wearied simply withstanding this whirlpool. It must stretch itself forward at all times not knowing what its future heralds while not lose its tensile strength to forbear the present. This predicament, though not new in its character, is certainly exceptional in its magnitude. For,

"But if they strive with thee to make thee ascribe a

partnership to that of which thou has no knowledge, then

obey thou them not. And accompany thou them in the World

according to what is fitting; but follow thou the path of him

who turns to Me. Then to Me is your return, and I will tell you

what you did."

~31:15, The Qur'an

Wisdom recommends that withdrawal from society, especially one so neurotic as today's and with all escape doors shut, does not make for successful living. The test may instead lie in the dictum of being with society without becoming of it, application of which in matters financial requires a thoughtful allocation of a small portion of savings to marketable securities.

Marketable securities, through the gyrations in the daily quotations that attach to them, reflect the contortions under-girding the political economy. The accumulated effect of these ephemeral price fluctuations, mediated through an ever evolving security market mechanism, is what allows a family to entwine its own balance-sheet to the current fluctuating fate of society it happens to find itself in, and in the measure it wishes to, for the better or the worse. In doing so, however, a family must take care not to be tripped over by the society it has chosen to dance with.

It may seem a paradox that that which symbolises the errors of society may also serve as a shield against those very errors. Or, in other words, the drug that addicts can also cure if it be administered in the right dosage.

For, so long as the structural winds of the political economy – as evidenced most in the dynamic dance of energy and credit – keep blowing with vigour, marketable securities have a role to play. And as and when that dynamic reaches its breaking point as it is wont to — for every few centuries every political economy revisits the grounds upon which it stands — it will send sufficient warnings in advance for society to take heed and make amends. And when the inevitable become imminent and the ship of society does indeed start to sink in the quagmire of its self-created, heedless and persistent pursuit of efficiency, matters far graver than money will stir the soul of a family.

It is precisely at such time that being on the right side of the law is what will hold most water over any other consideration. And it is also very much this quaint notion of adherence to law – specifically contract law – which rescues marketable securities from the dustbin of gambling and offers them a chance for redemption by reminding their owners that these securities are governed by the contract law.

For, as Nelson Nash fondly reminded that it is the contract law which underpins the fabric of every society; and history helpfully testifies that the written word, under common-law, has always carried weight when it comes to matters financial. It would seem strange, therefore, that in as information-a-heavy and literate-a-society as today's, the import of the written word, such as a security contract, should fail to carry fiduciary heft of some consequence.

But while the contract law rules the roost, it is also no denying the unseemly fact that every so often – in fact, more than what memory can hold – there arise episodic fits of subversion of this convention of 'rule by common-law' and common-sense. And it too is a fact that these episodes arise in no small measure and, at times, exclusively because of, regulatory negligence, complicity, or willful withdrawal of institutional safeguards.

Free rein, at such times, is provided to a select cohort to profit at the expense of all others: an act which, in times earlier, would have been castigated as nought but treason against the interest of the sovereign. Such subversions, though, do not subsist for long. They eventually lead to an unstable socio-political equilibrium, forcing a restoration, some times through means violent and brutal, whereby the written word is rediscovered, once again, and for some time, to prevail.

The contractual essence of marketable securities, thus, moves them beyond the unappealing realm of mere daily flipping of pieces of paper or bits of information; instead, it forces them to effectively codify a set of relationships that a family enters into with the society it happens to cohabit. In times today, rejecting them outright is a position difficult for a family to maintain for any considerable period of time without imparting damage of a permanent nature to the purchasing power of its property. But at the same time, the degree to which they be considered bears heavy caution: by committing a majority of its savings at their altar, the family opens itself to the charge of committing sacrilege of grandma's wisdom on money-management.

For, marketable securities are contractual promises and not contractual guarantees, and there always exists the temptation for one party to promise and the other to expect more than may be delivered, without question, the ultimate bane of all fame and fortune. As a result, marketable securities, by definition, harbour a peculiar risk called the counter-party risk — the risk that the party at the other end of a contractual promise fails to fulfill its end of the bargain because it found itself having entered into commitments with so many other counter-parties that, after a fashion, it was overwhelmed by the complex web of contracts it managed to carelessly weave for itself.

(N.B. This is no theoretical trivia: the follow-on repurcussions of the worldwide economic crisis of 2008, which was, in essence, a monetary crisis whereby a range of money-related contracts that underpinned world-wide money flows came undone, remain yet to be fully appreciated, understood and resolved. The world, it is safe to say, has not been the same since 2008, and if there was one proof needed of why contract law matters, the recent past makes for expert witness testimony.)

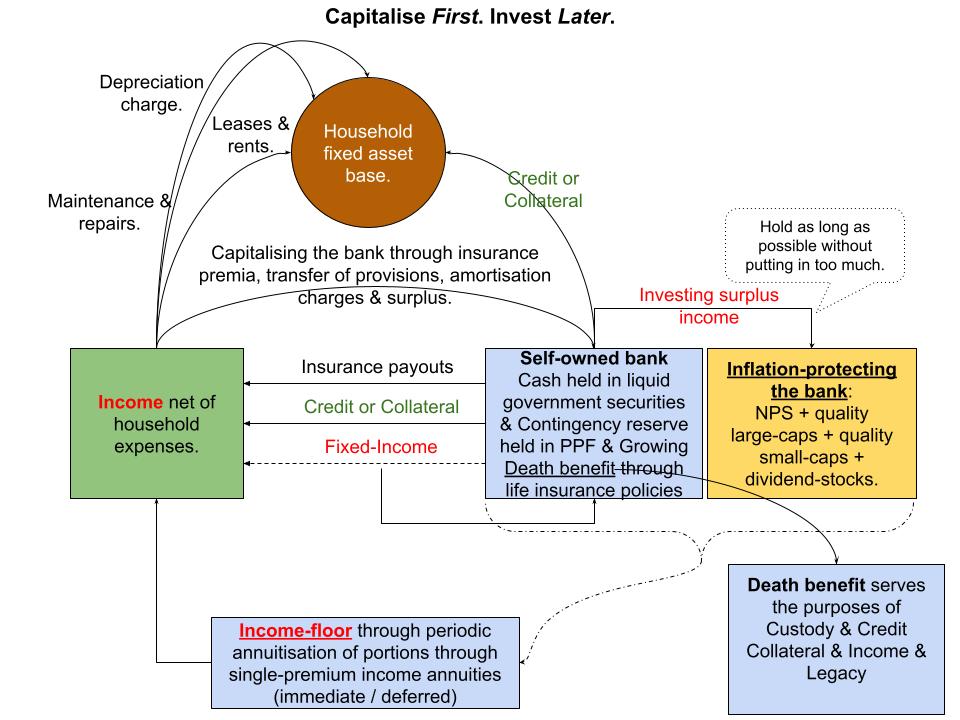

Nonetheless, just because the world changes in many aspects does not imply that traditional wisdom is in search for replacement: on the contrary, the resonance of its importance resounds even more loudly. All said and done, the idea of being a banker unto oneself (introduced towards the end of this primer), which tries to strike a middle ground between contractual guarantees and contractual promises, may remain the most sensible option to shelter savings for many ordinary families. For,

He who observes the wind will not sow,

and he who regards the clouds will not reap.

As you do not know the way the spirit

comes to the bones in the womb of a woman with a child,

so you do not know the works of God who makes everything.

In the morning sow your seed,

and at evening withhold not your hand,

for you do not know which will prosper,

this or that,

or whether both alike be good.

~~ Ecclesiastes 11:4-6

Why the NPS: warehousing of marketable securities

In light of the above lengthy digression, it is now possible to think of the NPS as part of a system-of-saving supplying the means whereby to attach a portion of the surplus capacity of a family's balance-sheet – its monetary savings – to claims of ownership on income-producing assets of other entities through purchase of their publicly-issued securities, and till such time these savings need to be converted back to income (through annuities). In order for any savings vehicle to play this role – one of capitalising savings through marketable securities – it needs to possess certain features which the design of the NPS seems to have captured.

To appreciate these features, it is worth recalling, once more, that a security is a legal entitlement of ownership (on an asset) under contract law. It is the contract law which, first and foremost, 'secures' the value behind a security, by providing sanction to the rights of the security holder, and abuse of which, in turn, can call into permanent doubt the worth of the security itself.

(N.B. This is different from, say an insurance contract, wherein the policy-holder is the true owner of the cash put in, and the insurance company is a custodian of that cash and is beholden to fulfill its contractual obligations, provided the policy-holder fulfills his own.

But even an insurance contract provides a weaker form of ownership than direct physical ownership of gold, an act which alone is free of all counter-party risk, thereby qualifying gold as the only true medium of inter-generational capital preservation.)

Now, the fact that most families will purchase marketable securities through some or the other intermediary – an Asset Management Company or brokerage – already weakens their ownership of the assets behind those securities. For, when money is transferred to an intermediary, it is that intermediary who buys the securities and is the actual owner of those securities.

As a result, those who contribute to, say, a mutual fund scheme have legally established a claim on the assets of the mutual fund scheme itself, and not the securities that the schemes owns in turn. Effectively, then, their ownership of those securities becomes one-step removed from true ownership (and that of the assets underlying those securities, a further two-steps removed).

With increased digitisation of information, it is hardly a surprise that over time this chain-of-distancing of ownership has expanded further, with the introduction of exchange-trade funds (or ETFs) being a case in point.

In the case of ETFs, a financial intermediary, essentially a Sponsor, buys an entire basket of securities and holds it on its own balance-sheet, acting as a warehouser of securities. The Sponsor then, with help of a specialised broker, issues a new type of security – called a share in the ETF parlance – which serves the office of a legal claim on this entire basket (of securitites). Thus, those who contribute to an ETF actually purchase these shares that are effectively created and issued by the Sponsor.

To an untrained eye the mechanics appear the same across both the mutual fund and the ETF: exchange some cash for claims. However, there is a paramount difference and that difference arises on the sequence of operations between these two schemes of intermediation.

In a mutual fund, the Asset Management Company collects monies, creates and issues units at a face value and then goes out into the market to purchase securities. It is these units that then become the property of the participant in a mutual fund undertaking.

In the case of an ETF, on the other hand, the Sponsor first assembles a basket of securities, and then creates and issue shares upon this basket. Furthermore, it then makes these shares tradeable by floating them on a public exchange, much like other publicly-traded securities. It is when others purchase these shares is when the ETF receives money.

This sequence makes it possible, in turn, for someone to purchase an ETF share in the morning, only to later turn around and sell that share in the afternoon, effectively trading an entire basket of securities without ever owning it in the first place. The underlying basket of securities remains unmoved on the balance-sheet of the EFT intermediary, since for every buyer there is a seller. And when none is found, it is that specialised broker who helpfully offers to buy it up, a function that is deliciously labelled "market-making".

Were it not for the legal sanction that this arrangement has received, anyone would be correct in conflating this whole operation with the dealings of a mafia cartel. But it is an unspoken law of finance that the more technical tools that make themselves available in the hands of money-dealers, they will, rest assured, find more and more creative ways to separate the saver from true ownership of his savings.

Where mutual funds were akin to buying a bag of different fruits and vegetables together, ETFs are like a grocer issuing receipts on a bag of fruits and vegetables. With mutual funds, one at least owns the bag; with the ETFs all one has are the receipts. Admittedly, the ETFs do have their uses in builing complex financial portfolios, improving trading liquidity, or insuring against risks related to liquidity (i.e. market-making).

While an intimate knowledge of these use-cases is hardly necessary in building a family's nest egg, they do highlight the fact that financial engineering is forever underway to create newer and newer methods to warehouse and trade marketable securities, and that some of these methods may create a substantial distance between owning a security outright and owning it through someone else. And critically, what on surface seems as only a legal distinction has a singular bearing on deciding on how to attach savings to marketable securities.

For, if the money of the family is in reality only a claim on the balance-sheet of an intermediary, who, in turn, establishes claims on actual income-producing assets, what matters most to any family is to choose the right intermediary; or, in other words, to assess the fiduciary capabilities of that intermediary. This, by no means, is an easy task: it is equivalent to finding the right business partner to trust for the long haul. A consideration of this nature therefore demands that the intermediary, such as the NPS, possess features that provide fiduciary surity.

Fiduciary surity

The first noteworthy aspect of the NPS is that, like the PPF, it is centrally regulated. Therefore, the savings held under its custody are governed by a set of publicly available, transparent and non-discretionary rules hosted at the website of the NPS Trust (https://www.npstrust.org) that seek to give a sense of safety for scarce capital. The additional fact that the NPS online user-interface provides an easy way to access all the pertinent information and execute all transactions, provides an added degree of comfort to its user: arguably, this interface is amongst the most easy to use 'investment interfaces' that exists today in India.

Now, the NPS, by design, has to provide custodianship to savings of millions for the longest period amongst all other competing market-linked savings alternatives. This period, stretching two or more decades, starts with the day contributions are made to the NPS account to when the contributor reaches the age of sixty or crosses the age of superannuation, whichever is earlier.

The knowledge that its savings can be held for a long time under the purview of a regulated custodian offers the family a paramount behavioural advantage: it allows itself to securely wean itself away from its savings. For, nothing could be better for a family's financial health than to put aside a portion of its savings and forget for as long as possible; and if there be a choice of only one market-linked security-warehousing instrument to opt-for, the NPS offers itself as a trustworthy default choice.

It also offers the distinctive benefit in disbursing of what has been accumulated. It is easier to acquire marketable securities whose prices jump around daily, but surprisingly difficult to get out of them. One reason simply is technical: one is never sure when is the right time to sell, which may result in needless hesitation.

But beyond this hesitation, which confronts the buyer of every asset, is a conundrum which confronts the owner of an asset: it is difficult to let go of what you have spent a life-time acquiring. This only goes to compound that initial hesitation, leading to confusion and then, inevitably to haste and error.

Surely a man goes about as a shadow!

Surely for nothing they are in turmoil;

man heaps up wealth and does not know

who will gather!

~~ Psalms 39:6

Against this hesitancy, the NPS provides a simple anti-dote through two sets of rules. One set (of rules) governs the rebalancing between different types of securities, and the second governs the withdrawal of the proceeds, both being covered in some detail later.

The withdrawal rules, in particular, force an effective liquidation of the accumulated savings at some point in time or another, depending on the age of the contributing family-member. This event of liquidation occurs irrespective of the prevailing market conditions and whether the funds accumulated are needed or not, leaving the family, in turn, with an annuity contract and a lump sum of cash in hand. The lump sum component may be withdrawn in its entirety, or in parts, or through some form of a systematic withdrawal plan. Meanwhile, if the contributing family-member dies prematurely then, upon death, the accumulated corpus is transferred to the nominee as a lump sum, unless the nominee opts for an annuity.

This is but one example of the characteristic, rule-based nature of the NPS that leaves a family little in way of choice, and it is always good to have a part of the volatile section of a family's balance-sheet governed by rules rather than discretion or emotion. For this reason, the NPS, like the PPF, may be considered an important pillar for construction of a family's balance-sheet and must, therefore, be attended to with care.

As an added point of comfort: government employees (Central and State) are compulsorily required to contribute a part of their salary to the NPS. This diktat by law ensures that the NPS is unlikely to be grossly mismanaged given that the financial future of public-servants too is tied to the quality of its operations. In other words, even if the NPS falls from grace, its fall may be comparatively tolerable.

Is the NPS tax-efficient?

Now, some financial arrangements are more tax-efficient than others if they reduce current or future tax liabilities in a legally-permissible, transparent and simple manner.

Taxes may either be waived-off or deferred. The waiver – more properly, exemption of taxes – is a rare ocurrence, and today in India, it is restricted to only three financial instruments amongst those accessible to all families: the balance held in the Public Provident Fund account and interest earned thereon; non-term life insurance policy proceeds provided the contributions to them meet specific qualifications; and the lump sum withdrawal made out of the NPS Tier 1 account at the time of its closure.

In lieu of the grant of this exemption by the Sovereign, all three instruments demand a minimum lock-in period. In addition, certain tax-free bonds issued by PSUs may make an appearance from time to time wherein the interest earned is exempt. However, seeing the burgeoning public deficits, their occurrence may be an increasing rarity, and thus they cannot be relied upon to build a financial plan.

(N.B. In fact, it is foolhardy to assume that the tax-exemption on these three instruments will persist for life and across generations. Public taxation is closely related to the underlying social contract which governs any polity, and every polity is constantly dealing with conflicting and competing interests. The choices it makes thus with regard to taxation are as much a political decision as an economic one. But whatever these changes, they are unlikely to be made on an ad-hoc basis.

For, in any civilised society it is not considered advisable to steal away benefits that have accrued from promises made in the past through tax legislation that has retrospective effect; but it certainly is possible to restrict future benefits of past actions. So, for instance, it is quite possible for a future political dispensation to remove tax-exemption from the PPF for individuals above a certain income floor, or those having accumulated a certain balance; or, for that matter, to rescind the 60% tax-exemption on the lump sum component of the NPS on contributions made after a certain date. The hand of every Sovereign is always very long, and it has a habit of not sitting still for long.

For any regular family though there is little it can do on this front except to recognise that such possibilities exist, and try not to get wedded too firmly to the comfort of tax-exemptions. Nonetheless, the broader point holds: some financial instruments and contracts happen to be more tax-efficient, or at least more tax-advantaged, than others due to Sovereign largesse.)

The mechanism of tax-exemption also relates to another aspect of the NPS: that of moving savings from one type of marketable security to another: typically from stocks to bonds and vice-versa. As discussed later, the NPS allows a family to allocate its savings amongst various types of securities contracts and typically, shifting from one to another requires first selling one contract, paying a capital-gains tax upon proceeds of the sale, and then purchasing another. Within the NPS these types of switches, though, are exempt from the reaches of capital-gains taxes.

(N.B. It may be countered that hybrid mutual funds, such as balanced funds, also enjoy this advantage. However, hybrid mutual funds do not allow the saver to actually decide the allocation and physically make the changes; instead, they do on the saver's behalf. Furthermore, such funds display a single consolidated Net Asset Value (NAV) unlike the NPS which has a NAV for each class of security that is owned.)

Taxes can also be saved by deferring their payment, i.e., what is due today can be paid tomorrow. For the purpose of accumulation, tax-deferral provides two advantages. First, by not withdrawing a portion out of today's savings to pay taxes, savings can continue to earn interest or grow in totality instead of on a reduced base. Furthermore, deferring taxes for as long as possible may subject the savings to a lower rate of taxation. For instance, the rate of taxation in old age coud likely be lower than in the 40's or 50's simply because of a lower overall income.

(N.B. One implication of the above is that those who wish to minimise taxes, should not automatically strive to withdraw the highest permissible amount in the Tier 1 scheme as a lump sum, unless they need the same. While this act of lump sum withdrawal may result in tax-exemption at the time of withdrawal, the proceeds will, in turn, have to safeguarded by attaching them to one or another financial contracts that may have higher-tax incidence (such as bank deposits).

An annuity, on the other hand, from the stand-point of taxation involves a contractual transfer of a lump sum to an annuity provider (lit. an insurance company) who converts it into a stream of smaller but regular cash income. The tax on this income, being taxable at the marginal rate, stands the chance of declining with increasing age.)

Given the above considerations then, is the NPS tax-efficient?

The answer is, surprisingly, that it depends. And what it depends upon is the attitude of the saver to the idea of a certain portion of the Tier 1 balance being forcefully converted to an annuity. For, forced annuitisation removes the right to direct that portion of the accumulated corpus to other uses, and instead, converts it into taxable income. (It is always possible to both defer this act of annuitisation or to purchase annuities that in turn defer their pay-outs, thereby further elongating the time at which this portion of corpus really is exposed to taxation.)

Even this would not be anathema except for the fact that forty-percent of the original contributions and the subsequent gains accrued on them are both annuitised and thereby exposed to taxation. Some may chose to view this as an incidence of double-taxation, especially if their original contributions to the Tier 1 account came from after-tax income. They would naturally be disposed to view their contributions being taxed twice: before they were put in and after they were taken out.

And it is understandable why this resistance may arise when comparable options of savings are considered. For instance, in the case of bank deposits only the interest is taxed, or in the case of mutual funds only the gains are taxed. In either case, taxation is not applied to the principal itself.

This act of forced annuitisation resulting in an incidence of double-taxation may not make a material difference to those in the lower income-tax brackets but would likely prove a sore point for those in higher tax brackets, who are likely to make larger contributions throughout their earning years, are more likely to be left with a larger accumulated corpus, and, therefore, naturally averse to a reasonable portion of their life-savings being compulsorily made subject to taxation.

This permanent life-long tax bill, even though it be in form of deferred taxation, wil be something the reasonably well-off are, therefore, prone to detest. They would naturally prefer instead to divert their savings to mutual funds and pay tax only on the capital gains so realised.

The system of taxation of the NPS Tier 1 account demonstrates one thing: it is fundamentally a savings-oriented instrument and not an investment. Savings, by definition, are done for a clear purpose — in the case of the NPS, to create a floor for income in old-age through following a consistent and conservative warehousing of financial securities. With respect to this purpose, annuitisation is a desirable feature and not a design flaw.

But there is a further subtler message within this system: essentially, those who have been fortunate to accumulate a larger corpus, will have to pay back a higher portion of it to society than those who have accumulated a smaller corpus. The forced annuitisation, in effect, is an instance of 'progressive taxation'. For some it may reek of socialism in the grab of a market-linked savings instrument.

To each family, then, its own political preferences. For those who view annuitisation as inevitable in their financial planning, the NPS is tax-efficient, while those who intend never to consider it, the NPS is not. If ever in the future this feature of annuitisation be removed, rest assured, the taxation-policy of the entire NPS Tier 1 account will likely undergo a significant overhaul: for, the Sovereign never relinquishes the right to tax in one form of another what it considers as due to society has to be paid back.

Broadly speaking then, the NPS (its Tier 1 account that is) is a boon for a vast majority of families who are likely to see lower marginal rates of taxation throughout their lives, while it is likely to prove a dilemma to those who are fortunate to earn more: a dilemma that they should consider themselves fortunate to have and one that they will have to learn to resolve for themselves.

Customising the NPS

This optionality and flexibility, however, attaches not only to the tax-efficiency of the NPS. Despite being rule-governed, the NPS is surprisingly customisable when it comes to choosing where to put money, with whom and when to close the account.

To begin with, the NPS allows a saver to choose from several fund managers. It is preferable to use a fund manager who handles monies of government employees, yet is privately-owned. The NPS allows shifting the managers not only for the entire pool of money, but also for individual investment categories. That is, it is possible to choose different managers for stocks, corporate bonds, government securities and alternative investments.

The NPS has two different types of accounts: a compulsory Tier 1 account to which all of the restrictions and tax-benefits apply; and, an optional Tier 2 account, which enjoys neither the benefits nor imposes any restrictions, i.e., it is open-ended. Indeed, as will be demonstrated later, it is the presence of the Tier 2 account, under the NPS umbrella, that enhances the utility of the overall NPS system by allowing for multiple use-cases.

Across both the Tier 1 and Tier 2 accounts, the cash contributed may be invested across four categories of securities: stocks or equity investments (E), corporate bonds (C), government securities (G) and alternative investments (A). Deciding how much of the contribution should go into which of these categories (components) is called defining the asset-allocation. For its Tier 1 account, the NPS provides either an auto or active choice when it comes to asset-allocation.

Under the auto-choice, the NPS rules automatically determine, based on the age of the contributor, how the current and future savings will be allocated, with more and more of the savings directed away from (E) and (C) to (G) with advancing age. In other words, from claims on private enterprises to funding of public budgets, and from securities with high expected short-term volatility to those with lower expected short-term volatility.

(N.B. The term expected refers to the fact that based on history, stock prices tend to gyrate more wildly than prices of fixed-income instruments such as bonds in time-frames ranging from 1 day to 15 years. Over 15 years though stocks by their very nature have proved a more reliable ally; but then not every family has the luxury of 15 years for all of their money.)

This auto-choice mode is helpful for many who have very little understanding or experience with market-linked securities. Within auto-choice, there are three types of sub-options to avail of with varying expected returns ranging from the highly conservative to slightly aggressive. Each of these three options differ in the rate at which they reduce the allocation to the (E) by the time the saver reaches the age of 60.

For instance, under the most conservative option (also called 'Conservative life-cycle fund'), the (E) component starts at 25% below the age of 35, and falls to 5% by the age of 55. Meanwhile, under the so-called aggressive option ('Aggressive life-cycle fund'), the (E) component starts from 75% and falls to 15% by the age of 55. The moderate option, as the name suggests, stands between the two, with the (E) component starting at 50% (at age 35) and falling to 10% by the age of 55.

While this has a seeming sense of scientific comfort, for those willing to self-educate themselves, the active choice is to be preferred. Though it is always possible to switch between the auto and active choices, it is preferable to make an informed choice at the time of opening of the NPS account itself. Those who are unsure should stick with auto-choice (preferably its moderate option), and when they gain more exposure and confidence may choose to switch to active choice.

Asset allocation

There is a theory that since the prices of stocks (which are but claims on current and expected surplus of a business operation) are highly volatile in the short-run, corporate bonds and government securities help to off-set that volatility. While true also in practice, care should be taken to not overdo the allocation to fixed-income instruments inside what is essentially a market-linked savings product; that too at an early-stage in life when several years of accumulation are still on the horizon.

In the short-run, while the prices of equity securities are certainly unpredictable — a fall of nearly fifty percent (50%), or more, within a span of a few weeks or months may not be ruled out — in the long-run they are more stable than fixed-income instruments. This, though, seems a contradiction: how can something which loses its sense of balance every day still manage to provide long-term stability? It certainly does not correlate with typical human experience.

An intuitive way to understand this is to realise that equity securities, or stocks, are claims on residual profits of public corporations, viz., profits which remain after everyone in sight has been paid-off, including the salaries of personnel, taxes to the Government, the lessors and the creditors. This feature of taking what remains is called 'optionality'.

It is akin to a party which runs on a rule that a particular individual will get the share of what remains at the end. With some shrewd planning and good-luck that particular individual may land-up with a fat share, and with luck, and stupidity, may be left with nothing. Now, imagine if this game is played everyday for several years and decades: in that case, what is the probability that this particular player actually acquires the largest share of the proceeds compared to all of the other participants?

A competent participant stands a good chance to maximise his share of the pie provided he can afford to be vigilant over all these years without fail. Stocks of sound corporations are like these competent participants; on the other hand, stocks of unhealthy corporations are like a participant found sleeping at the wheel, or engaging in deceit and fraud, for which they are eventually taken to task, even though more often than not it takes a long-time to take them to task.

It is this optionality which also gives stocks as a whole adaptability. Consider the participant in the party-example above: with years of experience, he acquires an enviable acumen to manoeuvre himself through the maze better than those who are simply content to take their fixed portions. In fact, the rules of the game leave him with no choice but to adapt as he will only get what is left over, so he better be extra-vigilant about safeguarding his interests.

In layman's terms: stocks as a whole are more adaptive to changing circumstances than bonds which by definition are contracts with fixed terms and conditions. It is this adaptability to long-term structural forces which enables stocks to bring a level of long-term stability to any portfolio of marketable securities.